Morning Note | Sept 22, 2022

Good Morning!

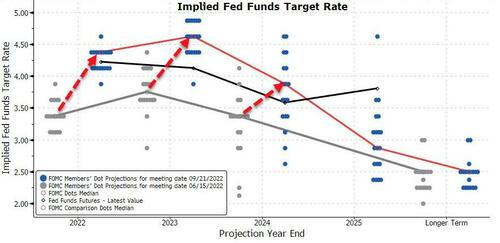

Stocks were slightly lower this morning with commodities higher and the dollar stronger. Yesterday, we received a hawkish revision to the dot plot: YE22 terminal rate increased from 3.375% to 4.375% and the 2023 dot went from 3.75% to 4.625%. Given this hawkish terminal rate, the market now sees 50bp hike in Dec FOMC from the previous 25bp and expects the terminal rate to be 4.5% early next year. The chances of a soft-landing have diminished.

The largest takeaway from the FOMC meeting yesterday was the change in the terminal rate to 4.6%. A higher terminal rate means more pressure on stocks. With the S&P at 3790, most of its gain from the July rally has been erased. The hawkishness of the presser continues to dominate the headlines. A higher-for-longer outcome means that recession risk is much higher.

In fact, Powell said as much saying that they would need the unemployment rate to rise to 4.4%, or 1m jobs lost, to hit demand hard enough to curb inflation. He also warned that the red-hot housing market is likely to suffer a correction as rates continue to rise.

In Powell’s prepared remarks, the most notable revision since the July remarks was to add that policy will likely be in a restrictive stance “for some time” and that history “cautions strongly against prematurely loosening policy.” In the Q&A, most of the questions were about risks of overdoing it, going too far, recessions, and pausing to assess policy lags. As for the conditions that would get the Committee to slow the pace of rate hikes or even pause, Powell gave three conditions: below-trend growth, softening in labor market conditions, and clear evidence that inflation is moving back to 2%.

"Below trend growth" is Central bank language for a recession. In my view, there is almost no chance we avoid one at this point. The question is, how deep will it be. Gundlach was on CNBC yesterday saying he believes it could be a deeper one and that stocks could fall to as low as 3,000 on the S&P 500.

The market fell by 1.7% in response to the Fed's hawkish projections. The steeper rate path than the one officials projected in June, highlights the Fed’s resolve to cool inflation and likely means further tightening in financial conditions, slower economic growth, and higher unemployment.

Also, we have to contend with souring sentiment, geopolitical tensions remaining high amid headlines that Putin will mobilize army reserves to support the Ukraine invasion, and a stronger dollar. Short-term bond yields rose, while the 10-year yield declined likely signaling more economic uncertainty ahead.

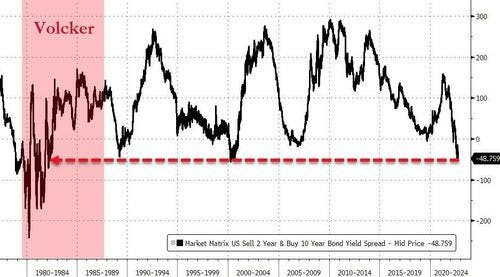

The inverted yield curve is now the most inverted since 1982 under Volcker.

CEF NAVs were surprisingly resilient yesterday with some equity areas down over 1% (in line with the market) but most fixed income sectors weathering the storm rather well. Muni NAVs were down only slightly, as were loans and multisector. But high yield and preferreds were actually up on the day. Discounts were mostly tighter on the day.

We didn't see much of a sell off in any funds. The CEF market may be flushing out the incremental CEF owner.

For those interested in adding risk, we would recommend keeping it in loans and high quality for now. Loans will benefit (somewhat) from the rising rates along with some mortgage funds that have floating rate assets (we have highlighted DMO in the past as an excellent option here).

In the loan segment, we like:

Eaton Vance Sr Floating Rate (EFV), 8.53% yield, -10.3% discount.

Nuveen Sr Income (NSL), 10.1% yield, -10.9% discount

Blackstone Long-Short Credit (BGX), 9.0% yield, -13.9% discount.

Pioneer Floating Rate (PHD), 9.5% yield, -13.4% discount.

BUY ALERT

Another fund to take a look at would be a term fund, BNY Mellon Alcentra Global Credit 2024 Target (DCF). I've talked about this one recently but I think it needs another discussion. The fund is slated to liquidate late 2024, so slightly more than two years. The tailwind yield, or the "yield" captured from the discount going away as it approaches that liquidation date, is over 4.1% per year. The yield is 8.5% on top of that so you're looking at an IRR in the low double-digits at this point.

It is extremely rare to see a term fund that has a high chance of being terminated trade so wide, so close to that date. Typically, within 4 years of liquidation, the fund tends to trade within 5% of the NAV if the distribution yield hasn't been cut to the bone.

The portfolio is a mix of different sub-sectors but the largest exposure is actually in the form of bank loans which are floating rate. The exposure is mostly from CLOs that the fund owns. These are junkier credits securitized into a single security.

The average bond price in the portfolio is under $85. That means that the loans have appreciation potential and is a large reason for the NAV to be so much lower this year.

We think the fund is a good option if you want to reduce your discount risk (risk that the discount moves wider) and potentially play the upside in the discount closing.

Have a great day!

----------------

Contact Us:

Admin@Yieldhunting.com

Latest Newsletter:

Google Sheet Models and Fund List

Model Portfolios (in progress- will post soon)

-----------------

Yield Hunting FAQ and Getting Started:

(A place to start for new subscribers)

-----------------

Data:

-----------------