Yield Hunting | December 2022 Newsletter

November was another good month with equities rising 5.4% while long-term bonds also rallied. A 60/40 portfolio did extremely well with both sides working.

The dollar finally fell hard providing that lift. The dollar is now the safe haven over treasuries and when it falls, money is flowing out into risk.

Inflation appears to have peaked and started its unwind lower. This is providing a lift to risk but also reducing interest rates supporting bonds as well.

Muni CEFs appear to have some NAV momentum and look compelling here. Most muni CEFs have cut at least once and now have wide discounts.

Take Advantage of End of Year Sale - 20% off our One Year Rates!

Remember, you still receive a free trial period and can cancel your membership at any time. You will receive access to all we offer: Models, Morning Notes, Weekly Recaps, and Monthly Newsletters… and above all, access to us! Reach us anytime via email with a response within 24 hours! You have nothing to lose… Try us!

”In economics, things take longer to happen than you think they will, and then they happen faster than you thought they could.”

- Rudi Dornbusch

Duration Has Gone From Enemy To Friend

Hyman Minsky wrote long ago that stability leads to instability. In other words, the more stable things become and the longer that they stay stable, the more unstable they will be when the crisis hits.

John Mauldin wrote several years ago about sand piles. Stay with me here.

We have all had the fun as kids of going to the beach and playing in the sand. Remember taking your plastic bucket and making sand piles? Slowly pouring the sand into ever bigger piles, until one side of the pile starts to collapse?

He used the analogy some research physicists compiled about what it took for the sand pile to collapse. They noted after several hundred iterations of building a sand pile until collapse that the pile was completely chaotic in its unpredictability.

Bring the analogy back to the markets. Markets tend to be 'fine' until they're not. And we're not talking small pullbacks or even orderly bear markets. We're talking about disorderly selling pressures.

The markets are currently expecting a soft landing with little in the way of earnings depreciation and job losses. They expect the consumer to remain robust.

But consumers can be laggy. And the Fed is on a mission to kill inflation. As the saying goes, 'don't fight the Fed.' They have control of the levers and all the power.

"The more resilient the consumer remains, the harder the Fed goes on tightening policy."

- Troy Gayeski

If the consumer remains resilient, the Fed will just move the terminal rate higher. The Fed will accomplish its goal- the question is the timing. Does it take longer than expected or does it happen quickly?

I would argue both. It will take both longer than expected but once it starts, it will happen very quickly with markets perhaps losing 10%+ in a very short time frame (week or two).

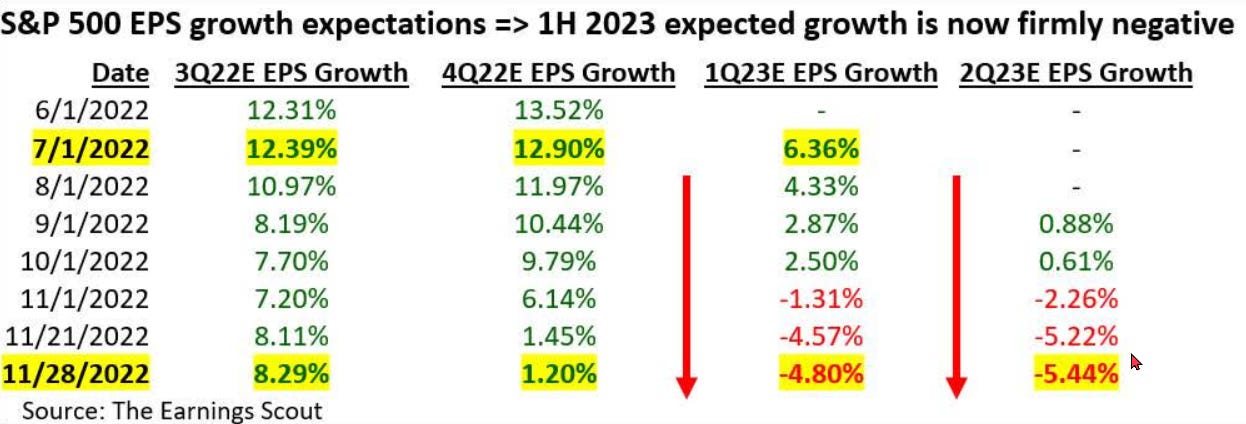

Third quarter earnings reports were horrible. Bottom-up estimates for the fourth quarter continue to decline.

In order to have a sustained asset recovery, the Fed would need to start cutting rates. While this will likely happen at some point next year, it is not likely near term. As long as central banks raise rates or keep them at current high levels, we believe assets will be rangebound with a more pronounced downside risk. Catalysts for a proper pivot (cutting rates) are likely some combination of increased unemployment, declining inflation, and something breaking in financial markets. As an increase in unemployment is not likely to happen very soon, markets will be on edge between waiting for better inflation data, slowing economy and earnings, and rising risks of a financial accident.

Breakevens in the TIPs markets (implied market-priced inflation rate forecasts) are showing a very rapid decline in inflation rates. Too fast in my opinion. They are priced to perfection for a sustained and fast drop in CPI to the Fed's target of 2.0%.

While the Fed could stick the landing- getting inflation to target quickly and then stabilizing it- it would be unprecedented. This would mean reducing inflation by a historic amount in one year. It strikes me as based more on hope and luck rather than probable.

Markets love stability and clarity. Right now, there is some stability with the Fed likely pausing hikes and greater clarity coming in for earnings. With higher rates discounting stocks lower, and declining earnings estimates, there is no footing below this market.

Stocks had to handle higher rates, which is why it was down in the first half of the year. Now we have declining earnings estimates. And we think earnings estimates which have been coming down slowly, could actually drop precipitously in early 2023.

This is the key behind our thinking that the recent rally is not an end to the bear market but just another rally like we saw this past summer. The S&P ended that rally just above 4,300. The lowest levels of the S&P this year is 3,577. We think we could retest those numbers and perhaps go below it.

The only way the recent rally turns out to signal that the worst is behind us is if the US somehow avoids a recession. But with monetary tightening (highlighted by a significant slowdown in money supply), avoiding a recession is unlikely. This is especially true when we add in the fact that much of the economy, especially in the goods sector, has to get back to normal after being artificially supported by trillions in temporary stimulus in 2020-21.

The impact of tightening financial conditions should build over time and is the main source of 2023 recession risk. However, we see a relatively low probability of a recession taking hold at the start of the year and forecast global GDP to expand at a 1.5%ar through 1H22, the same lackluster pace as recorded through the first three quarters of 2022. The near-term defense against recession comes, in part, from the resilience of healthy households and corporates that are relatively insensitive to rising rates. At the same time, we look for two important 2022 growth drags to fade, providing an important near-term defense against tighter financial conditions.

First, an unwind of inflation now underway is set to provide a material near-term growth lift. Aligned with evidence that pandemic supply bottlenecks have abated and global commodity prices have stabilized, a sharp drop in goods price pressures lowered CPI gains to 4.9% in the three months through September. This slide is even sharper in the US, where the dollar’s rise has pushed non-fuel import prices down for six consecutive months.

Any soft-landing scenario requires a balanced disinflation in wage and price inflation to be sustainable. While a stabilization in global commodity prices can be expected to shave more than 5%-pts off CPI inflation in the coming year, elevated wage inflation should prove stickier given tight labor markets and the building salience of the 2021-22 inflation surge.

Portfolio Positioning:

In summation, don't be a hero or get sucked in by FOMO. As JP Morgan said, "Nothing so undermines your financial judgment as the sight of your neighbor getting rich.”

Stay defensive! Don't get pulled into this market. Build a bench of dry powder while de-risking current positions into high-quality, high-coupon, bonds. We have been stressing this for months now. Duration was your enemy for the first 9 months of this year. It is now your friend.

Our take is that markets may continue to rally a bit until December (December 13th is the CPI report day) but have likely made the bulk of their run in this bear market rally.

We would use current and higher levels on the S&P to lighten up on risk assets including high-yield bonds.

The first half of next year could be a hard one. Earnings estimates could bottom in the first six months of 2023. That is when the market will likely hit its new lows.

This is when you can expect a Fed pivot, job losses, and much lower inflation.

A Fed pivot means lower interest rates and a bounce for bonds (barring wider credit spreads).

Portfolio Positioning - Introducing A Model of Models

*Members Only

Core Portfolio | Continued Defensive Posturing

*Members Only

Fun With Charts

(1) Covid cases in China are spiking

(2) QT starting to really ramp up.

(3) Chart of the month, in my opinion:

(4) Shelter inflation poised to take a dive dragging down core inflation.

(5) Morgan Stanley's Mike Wilson out with their S&P targets for 2023:

(6) JP Morgan and Morgan Stanley both say the era of the strong dollar is ending.

(7) The best time to invest

(8) Why CommishJW loves muni bonds!

(9)

(10) Emotions play a huge part of investing.

(11) Skill or luck?

Humor:

………..

This report included buys, sells, and other recommendations to Premium Members along with other guidance on where we see the markets heading…

Yield Hunting Premium Subscription

We always give a 7-day free trial to show what our service offers- don’t hesitate! Give us a try! And don’t forget our 10% of SALE!

Our strategy, simply put, is to create a portfolio of fixed income closed-end funds and alternative asset classes (such as REITs, Preferred Stock, and Baby Bonds) to create a risk managed approach to retirement income.

This approach can either be a standalone strategy (i.e- for most or all of your portfolio) or as a replacement for the failed 'fixed income' portion of your equity/ bond mix.

Either way, the goal is to create a safe income stream that meets as much of your monthly retirement expense needs as possible- thereby leaving the principle (as well as any equity positions) alone to grow unmolested. If selling is not necessary, we have effectively removed any or all sequence of returns risk from the portfolio.

We urge you to not miss this opportunity to take advantage of this really great offer. You really have nothing to lose with the one week free trial which locks you in at the lower rate.

This is a unique opportunity to create a fixed income closed end fund portfolio utilizing extremely rare discounts and high yielding securities. Yield Hunting can be utilized in various ways- to be the 'bond side' of your 60/40 diversified portfolio, your paycheck replacement strategy for retirement, or as a way to de-risk away from lofty equities and risky dividend stocks.

Our service utilizes Closed-End Funds, ETFs, Muni's, REITs, and Preferred Stocks to decrease risk, while still achieving a 8+% yielding, income-producing portfolio.

With a subscription to Yield Hunting, you get access to:

Our Three Portfolios that help create a safer and consistent 8% income stream:

Core Income Portfolio This is our main model. It has about a dozen securities (almost all CEFs) with almost no equity exposure. The risk profile by NAV is less than half that of the S&P 500. It is a bit more passive than most portfolios, with only a couple of trades per month- making it very easy to follow even for the novice investor. Current yield 8.3%.

Flexible Income Portfolio: This is our active trading portfolio. It is designed for more aggressive investors looking to maximize capital gains along with yield- looking for funds that have a high probability of mean reversion (extremely large discounts that have a good chance of closing in the short term). Current yield of 7.4% (some tax-free muni income).

Taxable Income Portfolio: This portfolio takes a more tax-advantaged approach, attempting to maximize after tax gains by utilizing funds that keep an eye on tax liability. Current yield of 4.9% (mostly tax-free).

Peripheral Portfolio Database: This is aimed at diversifying the Core Portfolio by investing in equity CEFs and REITs, preferred stocks, exchange-traded baby bonds, ETFs, Mutual Funds, and other securities. It is less a full portfolio than a list of researched funds that we recommend for those that want to expand beyond the conviction list of securities but don't have the time or inclination to do the research themselves. This includes a "Safe Bucket" section detailing the highest yielding cash-plus securities where excess cash can earn upwards of 4%. The model portfolios are designed with real time pricing detailing specific "buy, hold, sell" ratings.

Low Maintenance Models: This is for the pure, hands-off novice. In these models, you will assess your risk tolerance and can simply follow the model as you see fit within your risk profile.

Our premium service is organized in the following manner:

Morning Note - An almost daily note on the current situation in the market and what you need to know as the trading day starts.

Monthly Newsletter - Details the current investing environment, portfolio construction techniques and advice, and a review of our model portfolios. It is the perfect place to start for new subscribers!

Weekly Commentary - Goes through the events of the week and things to watch for in the upcoming week. This also includes performance of our holdings and the effects the current market situation will have on them.

Yield Hunting Review - this will take a more macro approach to the market for more long-term

Spotlight - Several write-ups each month, with specific analysis on securities we want to bring to our members attention where we see specific opportunities.

Alerts - Buy/ sell alerts on securities within the portfolio as conditions warrant

And finally....

Access - You are not on your own! We are available weekdays during market hours via email for any and all questions or concerns. We also offer a complimentary cursory review of your portfolio, so you know you are not going it alone and always have a professional's ear whenever you need it.

Why Yield Hunting?

While our service is aimed primarily at late stage career and retired investors, the strategy can also be used to lower risk by augmenting traditional equity investing via open-end mutual funds or ETFs. This includes those who have spent many hours researching and selecting the equity side of their portfolio, but don't have the knowledge or time to do the same for the fixed income side. We use high quality institutional research to avoid distribution cuts, opportunity risk, and other pitfalls which can derail your strategy.

Our Team

Three For The Price Of One! Being one of the larger services means we have a larger budget. We believe we've assembled some of the best talent on Substack and Seeking Alpha analyzing closed-end funds.

Our stacked team includes:

1) Alpha Gen Capital (Yield Hunting) - I am a career financial advisor (non-practicing) and investor. Not someone from another career doing this on the side. The AGC team and I use detailed analysis to provide safe and actionable insight without the fluff or risky ideas of most other letters. Our goal is to provide a relatively safer income stream with CEFs and mutual funds. Maybe more importantly, we also help investors learn about investing and how to properly construct a portfolio.

2) George Spritzer - Another career financial guru who runs a registered investment advisor with a specialization in closed-end funds for individuals. George uses the following investment strategies: 1) Opportunistic Closed-end fund investing: Buy CEFs at larger than normal discounts to NAV and sell them when the discounts narrow. 2) Exploit special situations: tender offers, fund terminations, fund activism, rights offerings etc.

3) Landlord Investor- Spent his career as a management consultant for public sector clients at a multinational consulting firm in the DC area. He has transitioned to a new career as a full time landlord. His investment portfolio is comprised of two parts -- broad-based index funds and income plays such as preferred stock, CEFs, and REITs. He also owns individual/baby bonds which he buys on margin to boost total return. Landlord is our 'individual preferred stock' expert analyst.