Weekly Commentary | Sept 11, 2022

Macro Picture

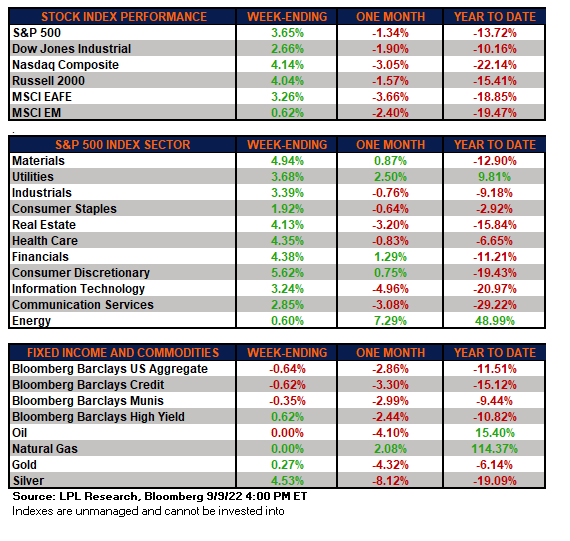

After three weeks of losses, the major equity averages posted nice gains of about 3-4%. Inflation fears subsiding a bit on lower oil prices was likely a catalyst for the rally but I would say short covering and a 'short squeeze' drove the significant gains. Essentially, the markets were oversold and due for a bounce.

With inflation running at 9.1%, the European Central Bank hiked its deposit rate from 0% to 0.75%, the largest hike in its history. ECB President Christine Lagarde suggested several more larger-than-normal hikes are likely and said inflation remains much too high.

The US had some dovish comments from a couple of Fed governors. Despite that, interest rates rose on the week slightly on the week with the 10-yr just below the highs of the last several years at 3.31% (high was 3.47% in March). Powell reiterated that his job was not done and that he hoped it could be done without 'high social costs' of higher unemployment.

The odds of a 0.75% rate hike on September 21st rose to 88% after Powell's remarks. Conversely, Federal Reserve Vice Chair Lael Brainard and Cleveland Fed President Loretta Mester also delivered comments that seemed to be more “dovish” than markets expected, with Brainard stating that she still believed the economy could avoid a recession as the Fed raised rates.

This all came together to help support the markets.

Obviously, the big event this coming week will be the Consumer Price Index (CPI) August figure out on Tuesday. We will see if inflation eased for the second month in a row. Watch for that headline number to fall but Core to rise.

The expectation is for +8.1% yoy for the headline number, down from +8.5%. Lower energy prices were largely responsible for driving down inflation in July, with the same likely in August as oil prices continue to decline. Shelter costs are likely to push up Core prices by +0.4%, up from +0.3% in July.

CEF Market Review

Discounts largely treaded water last week and haven't done much of anything in the last few weeks after that sharp tightening we saw in August dissipated. I haven't covered discounts and valuations in a while so I thought I would cover them a bit here.

Right now, the average fund is at a -4.6% discount- that's across all sectors and asset classes. Equity CEFs are much richer than the bond side with an average discount of -5.5%. While that is wider than the typical taxable bond CEF trading at a -4.4% or muni CEF at -3.5%, on a long-term historical basis, they are in the 21st percentile. That means that discounts have only been tighter 21% of the time.