Weekly Commentary | December 4, 2022

Macro Picture

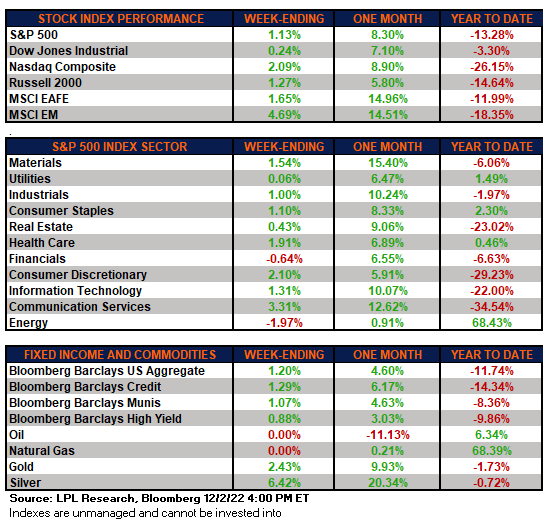

It was a good week for the markets as investors continue to bank on the Fed pausing or at least slowing the pace of interest rate hikes. The Fed chair took questions at a function he spoke at and reiterated that the Fed would be slowing the rate of increase. This helped interest rates come down for most of the week until the jobs report release on Friday.

The jobs report showed decent job growth of 263K with the unemployment rate staying at 3.7%. This was again above the estimate and helped to reverse the decline in interest rates. The 10-yr yield ended the week at 4.92%.

Both consumer confidence and PMIs, a gauge of manufacturing activity, are showing signs of weakening further. The PMI gauge fell to levels indicating that the manufacturing sector of the US economy is now in recession.

The lower yields is boosting the bond sector overall. Treasury yields are down nearly half a point in the last 6 weeks helping to boost bump the Bloomberg Aggregate Bond index by 3.7% in November.

Following last month's rally, the Dow is now up more than 20% from its October low and down only about 5% from its all-time high. Of course, that doesn’t reflect the broader weakness in equities, which is better reflected by the Nasdaq's 27% decline.

Investment grade just had their best month since 2008 as rates stabilized and moved back down. This helped municipal bonds have their best monthly return since 1986!

The S&P 500 has gained 17.4% from its low on October 13, the 5th notable rally since the peak back on January 4. The index closed above its 200-day moving average this week for the first time since April.

The market is betting on a soft landing but the chances of that are low. Just because the Fed stops raising doesn't mean that the market will magically stop going down and the economy not contracting significantly. Inflation will dictate what happens beyond that and when the Fed begins cutting.

Expectations for the terminal rate on Fed Funds have stabilized around 5.0% as the market is now matching the Fed in terms of rate hikes. Some firms are above 5.0% - Goldman is at 5.25%-5.50%- but for the most part, firms are matching that 5.0% terminal rate.

The question is, does inflation come down fast enough for the Fed to not have to raise more? That's something that is just a best guess at this point.

Monday: BEA Total Light Vehicle Sales (NOV), PMI Composite (NOV), S&P Global PMI Services (NOV), durable orders (Oct), factory orders (Oct), ISM Services (NOV)

Tuesday: Trade Balance (Oct)

Wednesday: Unit Labor Costs (Q3), Productivity (Q3), Consumer Credit (Oct)

Thursday: Weekly initial and continuing unemployment claims

Friday: Producer Price Index (NOV), University of Michigan Sentiment (Dec), wholesale inventories (Oct)

CEF Market Review

Taxable bond discounts continue to tighten and now are back inside the key -5% level at -4.84%. That is now 4 points tighter than the October 16th -8.84% level, a two standard deviation move. The discount percentile going back to 1996 is at the 60th. This is down from 94% at the peak nearly two months ago.

Muni discounts are at the 80th percentile with an average discount of -6.3%. While down from the peak, it is not down nearly as much.

This is counter-intuitive to me as the muni sector provides a degree of high-quality and safety in case of recession. The yields on individual muni debt is up around 4% on a yield-to-worst basis, from 1% on January 1.

Discounts, generally speaking, are not longer cheap cheap primarily because NAVs are stabilizing. Back in Oct, while discounts were much wider, the NAVs were still in free falls.