Weekly Commentary | December 18, 2022

Macro Picture

Stocks moved lower from their 200-day moving average last week as fears of higher rates fueling a recession spooked investors. We are back to early November levels on the S&P.

Two highly anticipated announcements during the week appeared to send sentiment in opposite directions—much higher at the start of the week and sharply lower at its end.

The first was the release of the Consumer Price Index "CPI" before trading began on Tuesday.

The data showed that inflation came down another 0.6% on the headline number to +7.1%. That is still remarkably high but trending in the right direction. We are back to December 2021 levels. Core inflation fell 0.3% from +6.3% to +6.0%.

At his post-meeting press conference, Fed Chair Jerome Powell stressed that in 2023 the central bank will not focus on rate cuts but instead on making policy restrictive enough to bring inflation down to its 2% target. Despite softer inflation readings recently, Powell said the Fed has “a ways to go” to return to price stability and that labor markets remain extremely tight.

The second big data point was the FOMC meeting where rates were raised 0.50% to 4.50% to 4.75%. The median forecast by members of the FOMC rose to 5.1% in 2023, higher than the median of 4.6% in September.

More importantly, the updated their economic projections showing Fed Funds reaching 5.125% by next December. Despite softer inflation readings in recent months, the committee raised its outlook for core PCE inflation to 3.5% from 3.1%. So, in other words, we saw the Fed come out and state that they have to raise rates further and despite that, inflation will be higher than they expect by the end of next year. A VERY hawkish outcome/statement.

The other notable surprise of the week may have been Thursday’s data on retail sales, which dropped 0.6% in November, defying expectations for a small increase and indicating a disappointing post-Thanksgiving “Black Friday” and “Cyber Monday” sales season. Sales in the previous two months were also revised lower.

Overall, the data this week reinforced that the economy is slowing and the Fed is going to keep up its aggressive stance, if not increase it, until inflation falls much further. More restrictive financial conditions will result in higher expected inflation than they thought previously.

Interest rates fell across the board which was paradoxical to what most people thought would happen. The interpretation could be that the market expects the Fed to keep going increasing the chances of a recession.

(More below)

CEF Market Review

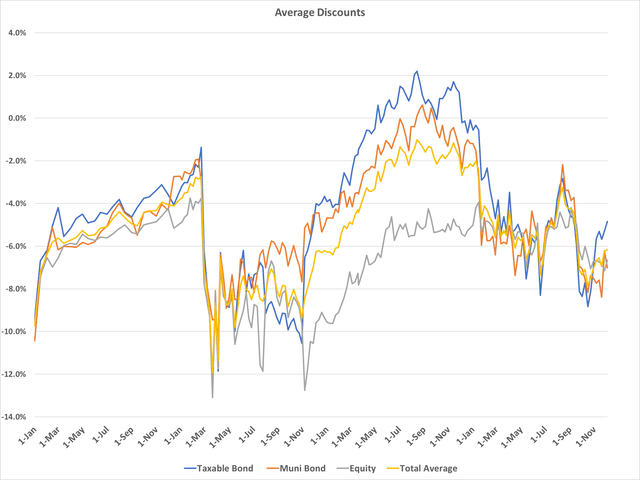

For the second week in a row, taxable bond CEFs widened out materially. As of the end of last week, taxable bond CEF discounts stood at -6.8% on average. From the Dec 4th nadir, discounts have widened by two points a little more than one standard deviation in fourteen days.

Taxables are back near the 90th percentile for average discounts. We were here about 6 weeks ago and then reverted back to the 50th percentile quickly. We have now made a full round trip.

We also saw muni bond CEFs widen as well from -8.4% to -9.4%. Muni CEF discounts have FINALLY reached the 95+ percentile in discounts. This is something we've been discussing for MONTHS now. In late 2018, muni CEF discounts reached the 99+ percent discount as the Fed was raising rates for the first time in over a decade.

We wondered how muni CEFs were not in the same spot today given the Fed was raising rates FAR more aggressively, inflation was out of control, and the sentiment in the bond markets was downright dismal.

In both segments- taxable and muni CEFs- discounts are finally looking compelling. The problem is that we feel taxable bond NAVs are set to decline materially next year. Despite the fact that we see the discount as an attractive buy, the NAV is NOT. And CEF investors should focus on buying the NAV, not the discount.

CEF sectors were largely lower on the week tough we had preferreds - a sector we actually highlighted as compelling just last week- outperform with prices up 1.25% and NAVs up 0.3%. The worst sectors were equity-related including dividend equity and covered calls all falling more then 2.5%.

From a valuation perspective, we continue to see our top focus categories of tax-free national munis, preferred, and taxable munis being the best values in this market. And these are the areas that we have stressed our members be focused on given our macro take of an impending recession, wider credit spreads, and eventually lower interest rates (another year or more away).

The market is giving us an opportunity here. Will you take it?

Keep reading with a 7-day free trial

Subscribe to Yield Hunting to keep reading this post and get 7 days of free access to the full post archives.