Weekly Commentary | December 10, 2022

Macro Picture

After touching the 200-day moving average, stocks have almost relentlessly retreated and have already given back most of the previous two weeks' gains. The largest driver was stronger economic data that undermined the chances of the Federal Reserve pulling back on their quantitative tightening and rate hiking.

We had the Producer Price Index ("PPI") surprised slightly to the upside coming in at +7.4% vs a +7.2% expectation. We also had the U of Michigan preliminary survey for consumer sentiment which was firmer than expected with long-term inflation expectations unchanged.

The 10-year yield declined a few bps and sits at 3.53%, a full 75-bps below the market -cycle highs. Oil has really been slumping falling another $9 to $72.50 from last week. The VIX is back over 20 rising all the way to 22.5.

Investors are watching closely two of the most important pieces of macro data this week: The Consumer Price Index for November will be out on Tuesday (830am EST) and the conclusion of the December FOMC meeting on Wednesday (~1215p EST).

After peaking at 9.1% year over year in June, CPI has edged lower four out of the past five months, and economists expect a further decline to 7.3% from the 7.7% level in October. Core inflation is expected to fall to 6.1% in November from October’s 6.3%.

Markets expect the Fed to raise rates next week by 0.5%, to between 4.25% and 4.50%, and eagerly await its so-called dot plot, which illustrates policymakers’ rate expectations along with their economic projections. On Thursday, the European Central Bank and the Bank of England meet; both are expected to hike rates by a half-point.

This bear market rally stalled that started in mid-October has petered out as investors see an impending recession ahead. The S&P is up approximately 11% in the past two months, while bonds are also up nicely at ~6% thanks to peaking, and subsequently falling, interest rates.

The biggest risk to the markets is the expectation on peak Fed Funds rates ("the terminal rate"). Since early November, the terminal rate has leveled off as market expectations and Fed dot plots converged.

If Tuesday's inflation comes in hotter-than -expected or if wages gains continue to move higher, you could see the Fed come out with more hawkish rhetoric forcing the terminal rate higher, and thus equities lower. We would also see bonds move lower amid interest rates moving back up and over 4.0% on the 10-yr.

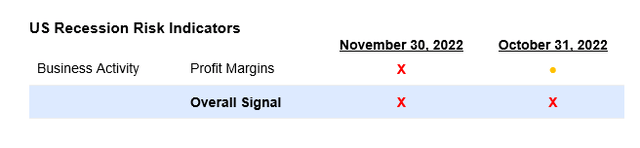

Franklin Templeton's Recession dashboard monitor has one more change negative for November with profit margins going from 'caution' to 'recessionary'.

CEF Market Review

Discounts widened out in the last week in a fairly significant move. For example, the average taxable bond CEF now trades at a -5.9% discount, almost a whole point wider. Muni bonds widened out by 1.3% on the week to -8.4%. Muni bond CEFs are now in the 92nd percentile of all observations. If you were holding out for some deals, they are now materializing. Perhaps some tax-loss harvesting was completed.

Taxable bond CEFs remain not all that cheap to us given the environment. If we do enter a recession, credit spreads WILL almost assuredly widen more from here as they sit in a relatively tight area of 4.5%. The Fed really wants these spreads to be tighter as part of their restricting of financial conditions to reduce inflation.

Keep reading with a 7-day free trial

Subscribe to Yield Hunting to keep reading this post and get 7 days of free access to the full post archives.