Weekly CEF Market Report - May 16, 2021

Macro Picture

We had our first wobble in a while as inflation fears sparked a large down day but the volatility proved short lived. Core inflation came in far hotter than expected which, when combined with last Friday's much weaker than expected jobs report, provided the spark that investors needed to finally sell. But the sell off lasted a whole day as the markets rallied hard on Thursday and Friday to moderate the losses.

Headline CPI (includes everything) rose to 4.2% over the last twelve months ending April 30. That was far higher than the 3.6% expected. This was the highest in nearly four decades. We also had producer prices get reported at +0.6%, double expectations.

But remember, this has a lot to do with the base effect and the year ago figures being so depressed. As we progress through the year, those numbers should start to moderate and by the fourth quarter, begin to head lower. The Fed stressed that inflation should "prove temporary" and that no shift in monetary policy was needed yet.

What was surprising is that yields only moved up slightly and then fell back a bit by the end of the week. Yields have not really moved all that much since the middle of March staying in a relatively tight 10 bps channel.

Commentary

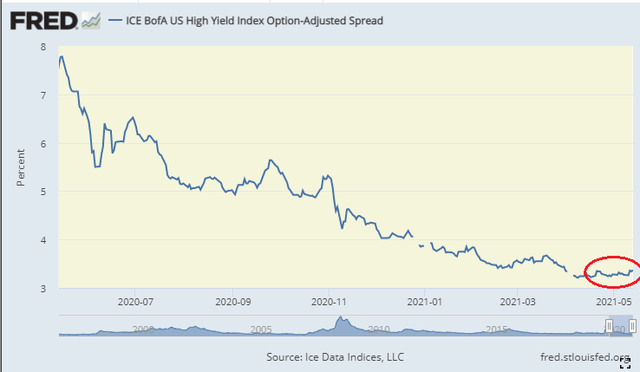

While discounts across the whole CEF sector widened, there were pockets of real weakness and pockets of strength. We saw a small creep up of the High Yield Spread index (a measure of risk for the general bond market) going from 3.25% (and very close to the tightest level) to 3.37%. While that small increase is almost immaterial in some respects, you can see what happened to NAVs last week.

High Yield CEF NAVs fell about a quarter of a point. What I'm trying to show is that you don't need a whole lot of widening to produce negative returns.

Even more important is that discounts on high yield CEFs widened by 0.45% on the week. That means, in addition to losing the 0.25% on NAV, the price fell by an additional 0.4% for a total loss across the sector of 0.7%. So a small wobble in the markets and you lost a month's worth of yield.

That is the problem with investing at these rich valuations.

And investing in funds that are trading at higher premiums (anything north of a +10% premium to NAV) is more problematic. As I noted in my CEF Report, those are the funds that investors tend to sell first. The PIMCO funds got slaughtered on Wednesday as investors dumped rich, higher yielding funds.

PCI and PCI lost 2.1% and 2.7% of their premiums this week. PGP and PHK lost 3.1%. PKO lost over 4% and PFL and PFN lost 3.8% and 2.1%, respectively. In the image above, RA, another high premium fund, lost 4.1% as well.

So does anything look attractive?

Not really. We have now seen these mini corrections in discounts a few times this year but this is the first since late March. But valuations remain very rich. I was surprised that the volatility didn't last more than a day. The spark for the correction was the CPI report which was far hotter than expected. Nearly all risk assets sold off. But a lot of the report was already priced in but I think it took the market a day to see that and flush out the trigger happy sellers.

CPI will continue to trend higher through the summer and likely peak around September. What is interesting is what the 10-yr did this week. If the inflation data was such a surprise, we likely would have seen the yield climb to new post-pandemic highs.

So I continue to "de-risk" extremely slowly adding more individual preferreds and notes (mostly preferreds of CEFs and BDCs) and waiting for better entry points in taxable CEFs. Since I get asked which positions I'm heavy in, here they are:

----------------

Yield Hunting Premium Members received a full list of funds in each sector- which funds we like here, and which to avoid...

----------------

Yield Hunting Premium Subscription

Our strategy, simply put, is to create a portfolio of fixed income closed-end funds and alternative asset classes (such as REITs, Preferred Stock, and Baby Bonds) to create a risk managed approach to retirement income.

This approach can either be a standalone strategy (i.e- for most or all of your portfolio) or as a replacement for the failed 'fixed income' portion of your equity/ bond mix.

Either way, the goal is to create a safe income stream that meets as much of your monthly retirement expense needs as possible- thereby leaving the principle (as well as any equity positions) alone to grow unmolested. If selling is not necessary, we have effectively removed any or all sequence of returns risk from the portfolio.

We urge you to not miss this opportunity to take advantage of this really great offer. You really have nothing to lose with the one week free trial which locks you in at the lower rate.

This is a unique opportunity to create a fixed income closed end fund portfolio utilizing extremely rare discounts and high yielding securities. Yield Hunting can be utilized in various ways- to be the 'bond side' of your 60/40 diversified portfolio, your paycheck replacement strategy for retirement, or as a way to de-risk away from lofty equities and risky dividend stocks.

Our service utilizes Closed-End Funds, ETFs, Muni's, REITs, and Preferred Stocks to decrease risk, while still achieving a 9+% yielding portfolio.

Get a One Week Free Trial Here: