Weekly CEF Market Report - July 11, 2021

Public Version

Macro Picture

The major equity indices were mixed on the week with the S&P up 0.4%, the Dow up 0.24%, and Nasdaq up 0.43%. But we had small caps down 1.1% along with MSCI EM, which was down 2.25%. A lot of the EM weakness can be attributed to China- who's crackdown on internet companies continues.

Here's a chart from Charlie Bilello:

Energy was the largest loser this week shedding 3.4%. Financials and Communication services were the other two sectors that lost money. Real estate and consumer discretionary were up 2.6% and 1.5%, respectively.

So value continues to pull back as rates continue to fall hitting five-month lows. Are we at the bottom though for rates? Hard to know but the steep decline early in the week was quickly bought and lasted but a few hours.

Economic data was also mixed with global PMI for June showed strength while the ISM services index slipped. The FOMC meeting minutes that came out on Wednesday didn't really create any reaction from market. The participants noted that they have not reached their goal of "substantial further progress" and suggested that the committee members are not in any hurry to begin tapering.

I still like value over growth here and think rates could inch back up. A lot of the recent drop is likely the Delta Variant scare. But what's interesting is you are not seeing a compliant move in utilities and other defensive equities. Typically, you see bonds and utilities highly correlated. In a "risk off" environment, bonds rise along with utilities (and other safe-haven equities or fall far less than the market).

That could mean that the move in the bond market is more technical than anything else and yields (along with the value trade) will resume this week.

Commentary

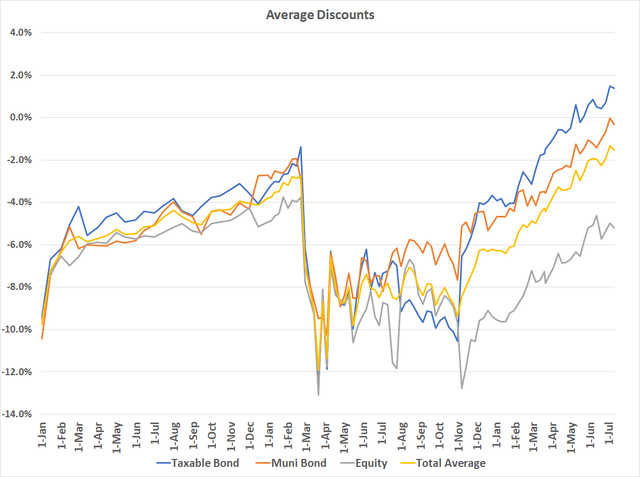

Discounts widened out small on the week with munis going from a small premium to -0.33% discount. Taxables were down a mere 5 bps. This makes sense given the rise in the Volatility Index ("VIX") this week from just under 15 to over 20, before ending around 16.2. This despite equities and bonds largely rallying on the week.

This shows that fear drives discounts more than anything. The fear of volatility- even if very short lived- can have a much larger effect than even positive price and NAVs. And I think that is what will ultimately drive discounts wider in CEFs; the fear that leverage costs will rise and the fear that spreads between CEF earnings and leverage cost drop (i.e. a flattening of the yield curve).

I spent a lot of time looking for needles in the haystack (hence the lack of many reports this week). I really wanted to find some place for investors to place some capital. Commish and I discussed this towards the end of last week and came up with a few ideas. I have a "Swap" article coming out in the next 24-48 hours that will also have some ideas for sells ---> buys based on relative value.

The relative value concept is one I have been discussing. A variation of it is buying the "higher yielding, wider discounted, better NAV performer strategy" (if people have a good name for this strategy I'm all ears!). Relative value looks for funds that have been widening in discount in the last 1-, 3-, 6- months while the rest of the sector is tightening.

Of course, in the last six months, few funds have seen widening so it mostly comes down, which funds have not participated in the rally. Nine out of ten of those "laggard" funds have a reason why they have not participated. Most likely it comes down to the distribution has been cut at least once. In other cases, fund performance has downright stunk.

But every once in a while we can find a fund that has relatively good performance, has not cut the distribution, and looks okay from a value perspective.

My top pick today would be..............

Yield Hunting Premium Members received a full list of funds in each sector- which funds we like here, and which to avoid...

We are currently running our Summer Sale Promotion. Subscribers receive 20% off the annual subscription rate! This is a limited time offer- lock in your lower rate now!

Yield Hunting Premium Subscription

Our strategy, simply put, is to create a portfolio of fixed income closed-end funds and alternative asset classes (such as REITs, Preferred Stock, and Baby Bonds) to create a risk managed approach to retirement income.

This approach can either be a standalone strategy (i.e- for most or all of your portfolio) or as a replacement for the failed 'fixed income' portion of your equity/ bond mix.

Either way, the goal is to create a safe income stream that meets as much of your monthly retirement expense needs as possible- thereby leaving the principle (as well as any equity positions) alone to grow unmolested. If selling is not necessary, we have effectively removed any or all sequence of returns risk from the portfolio.

We urge you to not miss this opportunity to take advantage of this really great offer. You really have nothing to lose with the one week free trial which locks you in at the lower rate.

This is a unique opportunity to create a fixed income closed end fund portfolio utilizing extremely rare discounts and high yielding securities. Yield Hunting can be utilized in various ways- to be the 'bond side' of your 60/40 diversified portfolio, your paycheck replacement strategy for retirement, or as a way to de-risk away from lofty equities and risky dividend stocks.

Our service utilizes Closed-End Funds, ETFs, Muni's, REITs, and Preferred Stocks to decrease risk, while still achieving a 8+% yielding portfolio.

With a subscription to Yield Hunting, you get access to:

Our Three Portfolios that help create a safer and consistent 8% income stream:

Core Income Portfolio This is our main model. It has about a dozen securities (almost all CEFs) with almost no equity exposure. The risk profile by NAV is less than half that of the S&P 500. It is a bit more passive than most portfolios, with only a couple of trades per month- making it very easy to follow even for the novice investor. Current yield 8.3%.

Flexible Income Portfolio: This is our active trading portfolio. It is designed for more aggressive investors looking to maximize capital gains along with yield- looking for funds that have a high probability of mean reversion (extremely large discounts that have a good chance of closing in the short term). Current yield of 7.4% (some tax-free muni income).

Taxable Income Portfolio: This portfolio takes a more tax-advantaged approach, attempting to maximize after tax gains by utilizing funds that keep an eye on tax liability. Current yield of 4.9% (mostly tax-free).

Peripheral Portfolio Database: This is aimed at diversifying the Core Portfolio by investing in equity CEFs and REITs, preferred stocks, exchange-traded baby bonds, ETFs, Mutual Funds, and other securities. It is less a full portfolio than a list of researched funds that we recommend for those that want to expand beyond the conviction list of securities but don't have the time or inclination to do the research themselves. This includes a "Safe Bucket" section detailing the highest yielding cash-plus securities where excess cash can earn upwards of 4%. The model portfolios are designed with real time pricing detailing specific "buy, hold, sell" ratings.

Low Maintenance Models: This is for the pure, hands-off novice. In these models, you will assess your risk tolerance and can simply follow the model as you see fit within your risk profile.

Our premium service is organized in the following manner:

Monthly Newsletter - Details the current investing environment, portfolio construction techniques and advice, and a review of our model portfolios. It is the perfect place to start for new subscribers!

Weekly Commentary - Goes through the events of the week and things to watch for in the upcoming week. This also includes performance of our holdings and the effects the current market situation will have on them.

Yield Hunting Review - this will take a more macro approach to the market for more long-term

Spotlight - Several write-ups each month, with specific analysis on securities we want to bring to our members attention where we see specific opportunities.

Alerts - Buy/ sell alerts on securities within the portfolio as conditions warrant

And finally....

Access - You are not on your own! We are available weekdays during market hours via email for any and all questions or concerns. We also offer a complimentary cursory review of your portfolio, so you know you are not going it alone and always have a professional's ear whenever you need it.

Why Yield Hunting?

While our service is aimed primarily at late stage career and retired investors, the strategy can also be used to lower risk by augmenting traditional equity investing via open-end mutual funds or ETFs. This includes those who have spent many hours researching and selecting the equity side of their portfolio, but don't have the knowledge or time to do the same for the fixed income side. We use high quality institutional research to avoid distribution cuts, opportunity risk, and other pitfalls which can derail your strategy.

Our Team

Three For The Price Of One! Being one of the larger services means we have a larger budget. We believe we've assembled some of the best talent on Substack and Seeking Alpha analyzing closed-end funds.

Our stacked team includes:

1) Alpha Gen Capital (Yield Hunting) - I am a career financial advisor (non-practicing) and investor. Not someone from another career doing this on the side. The AGC team and I use detailed analysis to provide safe and actionable insight without the fluff or risky ideas of most other letters. Our goal is to provide a relatively safer income stream with CEFs and mutual funds. Maybe more importantly, we also help investors learn about investing and how to properly construct a portfolio.

2) George Spritzer - Another career financial guru who runs a registered investment advisor with a specialization in closed-end funds for individuals. George uses the following investment strategies: 1) Opportunistic Closed-end fund investing: Buy CEFs at larger than normal discounts to NAV and sell them when the discounts narrow. 2) Exploit special situations: tender offers, fund terminations, fund activism, rights offerings etc.

3) Landlord Investor- Spent his career as a management consultant for public sector clients at a multinational consulting firm in the DC area. He has transitioned to a new career as a full time landlord. His investment portfolio is comprised of two parts -- broad-based index funds and income plays such as preferred stock, CEFs, and REITs. He also owns individual/baby bonds which he buys on margin to boost total return. Landlord is our 'individual preferred stock' expert analyst.