RiverNorth Specialty Finance: A 9.6% Yielder That Checks All Our Boxes

Summary

This is a unique interval fund CEF structure that allows investors to sell back a small piece of their shares at NAV quarterly. Think of it as a tender offer.

The fund changed its portfolio strategy to be more specialty finance as opposed to marketplace lending securities. The fund still has a small (<10%) allocation to those.

Most of the fund is invested in BDC baby bonds and notes. The rest is in other bond CEFs and BDCs.

They also have an allocation to CEFs as well as a large single whole loan to Square Inc.

This one checks all the boxes for what we are looking for in the "current" CEF environment for an allocation shorter term (<1 year) with strong NAVs, high yield, and decent discount.

I do much more than just articles at Yield Hunting: Alt Inc Opps: Members get access to model portfolios, regular updates, a chat room, and more. Learn More »

(This report was first issued to members of Yield Hunting on May 26th. All data herein is from that date. Since then, the price is up $0.11 and the NAV is up $0.03 which means the discount has closed by about 0.5%. There is still juice left here).

RiverNorth Specialty Finance (RSF) is an exchange-listed interval fund that invests in esoteric finance vehicles and securities. We'll go through what exactly it means to be an interval fund but wanted to start off with the fund owns and the investment objective.

The asset allocation of the fund is parsed between business development companies loans, small business loans, closed-end funds ("CEFs"), Asset-backed securities, and Business Development Companies ("BDCs"). They also have some investments in SPACs (specialty purpose acquisition companies).

(Source: RiverNorth Capital)

RSF is kind of a fund of funds with a large allocation to CEFs and BDCs (about a quarter of the fund) with an interval structure setup.

Fund Characteristics:

Total Assets: $141mm

Leverage: 31.6%

Structure: Interval Fund

Liquidity: Quarterly repurchase offer 5% to 25% of shares

Distribution: Monthly

Distribution rate: $0.1523

Distribution yield: 9.88%

What Are The Asset Backed Securities?

Asset backed securities or "ABS" can really be any liability that is backed by some sort of asset. Essentially, to keep it simple, some loans or receivables are transferred from the lender to a new special legal entity. The entity then packages up these loans and receivables into a new single security, through a process called securitization.

Securitized assets can include certain types of mortgages, commercial loans, automobile loans, student loans, bank loans, accounts receivables from a business, or credit card receivables. The new security then is sliced into tranches of varying risk as the top tranche is paid first, second tranche second, and so on.

(Source: SoFi)

The vast majority of the time, ABS are floating rate coupons. For instance, if you think of your credit cards, the interest rate charged to them goes up when short-term interest rates rise. But remember, SHORT-TERM rates need to rise, not long-term rates as most of these loans are based on some form of libor; typically 30-, 60-, or 90-day libor.

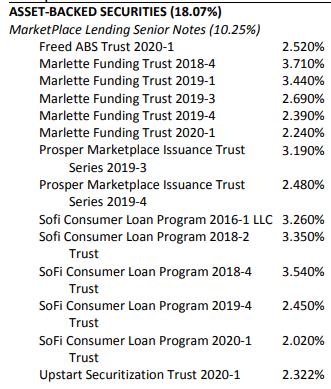

In the case of RSF, the fund owns just a few different flavors of ABS. Most of the securities are personal loans either from the purchase of some kind of good/service or from student loans.

Marlette Funding are Best Egg personal loans, mostly to individuals. These loans are typically for debt consolidation (you often hear these ads on the radio), credit card refinancing, or home improvement loans.

(Source: RiverNorth)

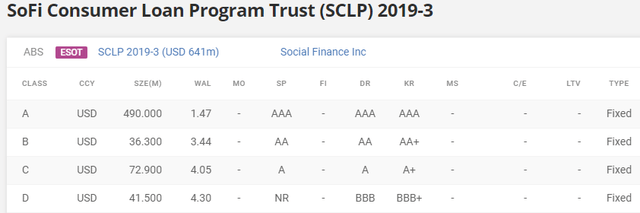

The SoFi consumer loan program is much the same thing. These are loans that may be formerly student loans and other debt consolidated into one SoFi loan. The entire company SoFi was founded and built around making education funding more affordable.

These securities are great areas for investment. They are relatively lower risk, even in the lower tranches. Risks on these holdings are mostly investment grade but the yields are lower as well. There's no free lunch. But what this does do is provide a bit of a hedge to short-term rates rising as most of the securities are floating rate.

What Are Business Development Notes?

This is the largest segment of RSF- essentially BDC notes- at over half of the portfolio. These are just individual bonds with some baby bonds mixed in there. Some BDCs use more traditional senior unsecured notes (bonds) to provide them their leverage instead of listed baby bonds. These are very similar to an individual corporate bond whereas a baby bond is a listed (has its own ticker) on an exchange.

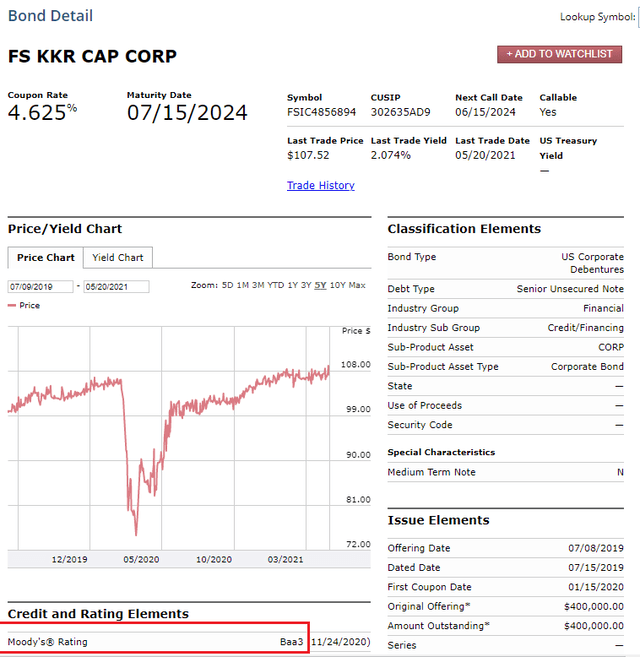

For example, here is the FS KKR Cap Corp 4.625% note off the FINRA website ("HERE"). These notes are not much different than most BDC baby bonds.

Most of these notes are investment grade.

I use BDC Buzz's sheets for these notes as an easy way to aggregate and analyze them. You can see most have strong interest coverage and asset quality. Maturities are all within 5 years with most nearer than that. You can purchase these via Fidelity's retail site by the way. RSF bought many of these in the downturn last year but now most are trading at or above par given the interest rate moves and risk asset recovery.

(Source: Sustainable Dividends, BDC Buzz)

What CEFS Do They Hold and Do You Like Them?

Their largest position at the start of the year was Barings Global Short Duration (BGH), a fund we still like today. They also own a bunch of floating rate including FSLF, VVR, JQC, EVV, and ISD.

I see nothing wrong with the holdings in their portfolio and they are/were well positioned for the rising interest rate environment.

(Source: RiverNorth)

The CEF portion of the portfolio is about 20% of the total which is down from the start of the year. On January 1, the fund had 20% in CEFs and another 18% in BDCs for a total of 38% between the two. Today, according to the most recent fact sheet dated March 31, they had 21% in aggregate between the two. This makes sense given how hard they've run in the first quarter of this year.

What Else Is In There?

Lastly, they have 8% in SPACs (special purpose acquisition companies) which have been all the rage in the last two years. These are "blank check" companies that IPO like a stock and then, within the parameters set forth in the prospectus and rules surrounding these securities, go out and acquire either a public or private company. Most of these have been hit hard this year and are "on sale."

The other position on the initial image from the fact sheet is the "Small Business Whole Loans." I'm not sure why they pluralized "loans" since there is just one loan accounting for 21% of the portfolio. From the semi-annual report:

(Source: RiverNorth)

So the company has just one whole business loan from Square (SQ). That is a bit of risk added to the fund given the concentration. SQ is a solid financial transactions processor but anytime you have 21% in one security you have a lack of diversification to some extent which adds to your risk.

The Distribution And Valuation

The company raised the distribution at the start of this year going from $0.1453 to $0.1523, an increase of 4.8%. Anytime a fund raises the distribution, you know there is a bit of safety to it. The fund actually earned far in excess of that $0.1523 per month in the last six months of 2020 and the UNII value rose to a whopping $1.173. This was largely from the shift in the portfolio strategy last year juts as the Covid Crash was occurring (lucky!).

Last July the distribution was cut from $0.18 to that $0.1453 as the fund deleveraged like many other funds.

As these notes and other securities have largely recovered, the earnings and UNII growth is not likely to continue. Still, there is a heck of a lot of cushion there so we have nearly zero concerns about the distributions so long as another monster crash doesn't occur- then all cards are off the table.

CEFdata puts the fund in the loan category which is where we would put it as well. The fund stacks up well against the category with a strong NAV performance.

The fund is still trading at a -6.25% discount which I think is a reflection of investors' hesitation with not knowing exactly what they own and about the interval structure. We do think RSF will trade much closer to par given the yield and NAV performance. It will take time though as investors need to get more familiar with interval fund structure and what are BDC notes, small business loans, etc.

Interval Structure Means What?

So what is an interval structure actually mean? We recently reported that VTA, under attack from Saba, is converting to an interval fund. And we think this is going to be more common in the future as fund sponsors want to be able to reduce the discount without giving daily liquidity.

As an interval fund, they repurchase 5% to 25% of outstanding shares quarterly at NAV. Each shareholder gets a mailer for up to 5% in December, March, June, or September for a repurchase the following month. Essentially, thing of this as a quarterly tender offer for 5% of shares.

This helps to reduce the discount because you can sell back a portion of your shares each quarter and capture a gain. If the market were truly efficient, the discount would be fairly tight since you could just sell your 5%-25% of shares each quarter and quickly repurchase the shares sold in the market at a discount.

Concluding Thoughts

The fund is a unique portfolio that you won't find in most of the rest of the CEF market. This is something that only can be held in a closed-fund structure due to the illiquidity of the holdings. The quarterly tender is also fairly unique and could be a source of alpha at these discount levels.

But right now, this one checks a lot of the boxes for at least a shorter-term holding (3-9 months) with strong NAV momentum, a higher yield (this one is actually covered), and a decent discount.

Yield Hunting Premium Subscription

Our strategy, simply put, is to create a portfolio of fixed income closed-end funds and alternative asset classes (such as REITs, Preferred Stock, and Baby Bonds) to create a risk managed approach to retirement income.

This approach can either be a standalone strategy (i.e- for most or all of your portfolio) or as a replacement for the failed 'fixed income' portion of your equity/ bond mix.

Either way, the goal is to create a safe income stream that meets as much of your monthly retirement expense needs as possible- thereby leaving the principle (as well as any equity positions) alone to grow unmolested. If selling is not necessary, we have effectively removed any or all sequence of returns risk from the portfolio.

We urge you to not miss this opportunity to take advantage of this really great offer. You really have nothing to lose with the one week free trial which locks you in at the lower rate.

This is a unique opportunity to create a fixed income closed end fund portfolio utilizing extremely rare discounts and high yielding securities. Yield Hunting can be utilized in various ways- to be the 'bond side' of your 60/40 diversified portfolio, your paycheck replacement strategy for retirement, or as a way to de-risk away from lofty equities and risky dividend stocks.

Our service utilizes Closed-End Funds, ETFs, Muni's, REITs, and Preferred Stocks to decrease risk, while still achieving a 8+% yielding portfolio.

With a subscription to Yield Hunting, you get access to:

Our Three Portfolios that help create a safer and consistent 8% income stream:

Core Income Portfolio This is our main model. It has about a dozen securities (almost all CEFs) with almost no equity exposure. The risk profile by NAV is less than half that of the S&P 500. It is a bit more passive than most portfolios, with only a couple of trades per month- making it very easy to follow even for the novice investor. Current yield 8.3%.

Flexible Income Portfolio: This is our active trading portfolio. It is designed for more aggressive investors looking to maximize capital gains along with yield- looking for funds that have a high probability of mean reversion (extremely large discounts that have a good chance of closing in the short term). Current yield of 7.4% (some tax-free muni income).

Taxable Income Portfolio: This portfolio takes a more tax-advantaged approach, attempting to maximize after tax gains by utilizing funds that keep an eye on tax liability. Current yield of 4.9% (mostly tax-free).

Peripheral Portfolio Database: This is aimed at diversifying the Core Portfolio by investing in equity CEFs and REITs, preferred stocks, exchange-traded baby bonds, ETFs, Mutual Funds, and other securities. It is less a full portfolio than a list of researched funds that we recommend for those that want to expand beyond the conviction list of securities but don't have the time or inclination to do the research themselves. This includes a "Safe Bucket" section detailing the highest yielding cash-plus securities where excess cash can earn upwards of 4%. The model portfolios are designed with real time pricing detailing specific "buy, hold, sell" ratings.

Low Maintenance Models: This is for the pure, hands-off novice. In these models, you will assess your risk tolerance and can simply follow the model as you see fit within your risk profile.

Our premium service is organized in the following manner:

Monthly Newsletter - Details the current investing environment, portfolio construction techniques and advice, and a review of our model portfolios. It is the perfect place to start for new subscribers!

Weekly Commentary - Goes through the events of the week and things to watch for in the upcoming week. This also includes performance of our holdings and the effects the current market situation will have on them.

Yield Hunting Review - this will take a more macro approach to the market for more long-term

Spotlight - Several write-ups each month, with specific analysis on securities we want to bring to our members attention where we see specific opportunities.

Alerts - Buy/ sell alerts on securities within the portfolio as conditions warrant

And finally....

Access - You are not on your own! We are available weekdays during market hours via email for any and all questions or concerns. We also offer a complimentary cursory review of your portfolio, so you know you are not going it alone and always have a professional's ear whenever you need it.

Why Yield Hunting?

While our service is aimed primarily at late stage career and retired investors, the strategy can also be used to lower risk by augmenting traditional equity investing via open-end mutual funds or ETFs. This includes those who have spent many hours researching and selecting the equity side of their portfolio, but don't have the knowledge or time to do the same for the fixed income side. We use high quality institutional research to avoid distribution cuts, opportunity risk, and other pitfalls which can derail your strategy.

Our Team

Three For The Price Of One! Being one of the larger services means we have a larger budget. We believe we've assembled some of the best talent on Substack and Seeking Alpha analyzing closed-end funds.

Our stacked team includes:

1) Alpha Gen Capital (Yield Hunting) - I am a career financial advisor (non-practicing) and investor. Not someone from another career doing this on the side. The AGC team and I use detailed analysis to provide safe and actionable insight without the fluff or risky ideas of most other letters. Our goal is to provide a relatively safer income stream with CEFs and mutual funds. Maybe more importantly, we also help investors learn about investing and how to properly construct a portfolio.

2) George Spritzer - Another career financial guru who runs a registered investment advisor with a specialization in closed-end funds for individuals. George uses the following investment strategies: 1) Opportunistic Closed-end fund investing: Buy CEFs at larger than normal discounts to NAV and sell them when the discounts narrow. 2) Exploit special situations: tender offers, fund terminations, fund activism, rights offerings etc.

3) Landlord Investor- Spent his career as a management consultant for public sector clients at a multinational consulting firm in the DC area. He has transitioned to a new career as a full time landlord. His investment portfolio is comprised of two parts -- broad-based index funds and income plays such as preferred stock, CEFs, and REITs. He also owns individual/baby bonds which he buys on margin to boost total return. Landlord is our 'individual preferred stock' expert analyst.