Morgan Stanely EM Debt Funds: An Alligator Mouth Opportunity

We have been positive on emerging market income closed-end funds (”CEFs”) for some time, preferring the most heavily exposed to local currencies. In this report, we go through the current opportunities and why this is one of the areas of the CEF taxable space we like today.

We like two opportunities in the space which pair well together.

Practical Takeaways:

Treat EDD and TEI as “unhedged by design” currency exposure, and treat MSD and EMD as US dollar credit you can hold without a currency prediction. “Hedging” in this group is a positioning tool, not a risk-removal tool.

If the dollar doesn’t fall (”Warsh effect”), then the MSD exposure should be a nice hedge.

Owning the two simultaneously will reduce - significantly- the amount of currency exposure the dual-position portfolio is susceptible to.

The EM Income CEF Space

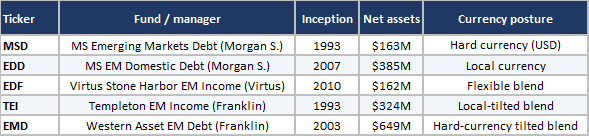

These are all five CEFs that we classify as the emerging market income sub-group. They have a diverse set of currency mandates, which is the primary layer in which to analyze.

The funds have been around for some time with EDF being the youngest of the funds at 16 years. Three of the five have been through several iterations of mergers and takeovers.

For example, EDF absorbed sister fund EDI in the most recent corporate action among the group back in 2023. EMD merged two sister funds when Franklin bought Legg Mason back in 2020. EDD is the cleanest of the funds with no mergers or renames.

Let’s Walk Through the Funds

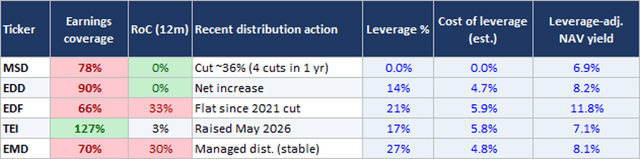

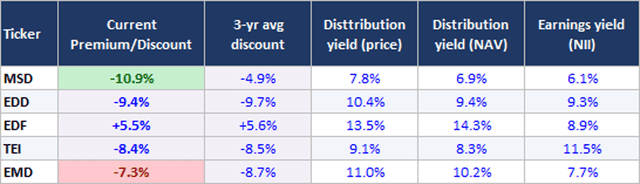

The yields vary from 7.8% on MSD to 13.5% on EDF with earnings yield not really being indicative of those payouts. TEI has the highest earnings yield but the second lowest distribution yield.

EDF and EMD have the highest distribution yields but they are juiced preferring to pay out some return of capital (”roc”). That is captured with a higher valuation as well.

MSD is the only fund without leverage but all but EMD have fairly modest amounts of borrowing.