January 2024 Newsletter | LOCK IT IN!!

Summary

The narrative has not changed but we are progressing through it. The long-await pivot has arrived and we have now fully priced that in along with the soft landing.

My thoughts/thesis are simple: We likely see some semblence of a harder landing next year while inflation continues to fall - with rates falling faster.

A more prolonged slowdown is likely in 2025 as the government is forced to slow spending growth. That should push down rates a bit further.

In summary, we see upside risks to rates and downside risks to growth. Focus on bonds over stocks, international over domestic, small over large caps.

Muni CEFs are our top trade idea for 2024. We think the risk-return could be massive with the potential for 30%+ total returns.

(This is rare a free posting of our regular monthly newsletter. For additional insights, help with your portfolio, and more in depth converage of closed end funds, bonds, and preferred stocks, consider subscribing)

"For 2024, I'm going with Muni funds [CEFs]"

- Peter Tchir

The combination of overbought financial assets and frothy valuations means that the future returns we discussed in the September letter are even more dour. The massive liquidity injection of 2020-2021 pulled forward years of returns, I fear.

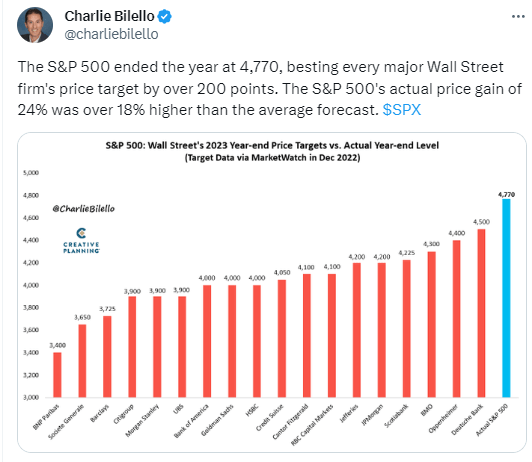

The most crowded trade according to the BofA Fund Manager Survey is long the Magnificent 7. It beats out the short China trade by a wide margin.

The narrative has not changed but we are progressing through it. The long-await pivot has arrived and we have now fully priced that in along with the soft landing. Any deviation from that path means markets are susceptible to a fall.

The economy continues to defy expectations of a recession- or even a slowdown. Inflation has been moderating and remains on track to fall in line with Fed targets later in 2024 or early 2025.

I still see the downside risks being far greater than the upside surprise potential in 2024. The possibility of a soft landing remains 50/50 at best but rates are likely to stay higher for longer despite the cuts projected for this year. That is likely due to the large new supply of treasuries coming to the market in 2024.

Right now the market is pricing in DOUBLE the amount of cuts that the Fed is projecting. That's another risk if that doesn't come to fruition.

My thoughts/thesis are simple: We likely see some semblence of a harder landing next year while inflation continues to fall- with rates falling faster. A more prolonged slowdown is likely in 2025 as the government is forced to slow spending growth. That should push down rates a bit further. In summary, we see upside risks to rates and downside risks to growth.

Takeaways:

The Fed will likely cut rates quickly but the risk is that they don't cut as fast as the market expects. It will be difficult for them to cut faster so the risk is to the downside there.

Corporate margins are falling thanks to de-globalization and shipping concerns coupled domestically with wage costs as the advantage shifts from corporate to labor. Reduce Low moat equity exposure

International stocks are now extremely cheap relative to US stocks- about as cheap as they've ever been. And interestingly, the larger the better the relative valuation. Long: EFA & EEM, short SPY

Bonds look very favorable relative to stocks, especially US stocks. The implication would be to shift the asset allocation from stocks to bonds but within stocks, according to the last bullet point, shift to international, especially emerging markets. Long: EDV, IGLB, SPLD, FIGB

In bonds, keep up quality like investment grade bonds. The allocations made to treasuries over the prior months look to be well-timed but now you must be willing to take yields sub-4.0% to lock in yields for more than 5 years. Long: IGLB, FIGB, FCOR, BSCX

In CEFs, discounts remain very wide in munis and we think that remains the trade for 2024. The top picks change daily so follow the daily notes and Weekly Commentaries but for the most part, you could throw a dart or follow Saba's lead. Long: NMZ, NMCO, RFMZ, BMN, ETX, MMD

We would continue to avoid higher-risk, lower quality areas of the bond market, especially within CEFs as a new default cycle has started. I see relatively no advantage for going into the lower quality areas of the bond market on a risk-adjusted basis. Spreads are just too tight. Avoid high yield and reduce floater exposure

The Mag7 stocks look very reminicent of the Nifty Fifty from the 1970s. Today, they sport an average P/E of more than 50x earnings. This for companies that are already $2T+ in market cap. This is being fueled by AI euphoria. Underweight Mag7

The story of 2024 will be the end of the inflation story and the focus on cutting rates while growth slows dramatically. It is also an election year which means there will be a lot of diversions out there to the markets.

As core inflation is on track to return to the 2% target by the middle of next year, we expect the Fed to cut interest rates by 25bp at every meeting next year from March onwards, with rates eventually falling to between 3.00% and 3.25% in early 2025.

'This time is different' continues to be discussed in the media and while likely true to some extent, it often rhymes with history and past parallels and relationships eventually hold true. Excessive liquidity from Covid is likely delaying, not obviating, those traditional relationships.

From Kurt Altrichter:

This is indicating that officially something is “different this time.” Yet, this doesn't guarantee a different end result. While we're witnessing a record-breaking rally post-inversion, the future remains unpredictable.

Considering the yield curve's consistent success in predicting recessions and the following equity bear markets since the 1950s, history says the risk of a significant and painful drawdown looming ahead is near 100%.

So what is different this time?

The tsunami of cash. Literally, the Federal Reserve and Congress together created a figurative tsunami of stimulus. In essence, the combined central banks of the world tossed three decades of money supply into the system in a mere 16 months. It is just not possible for that NOT to distort all economic theory- at least for a time.

The question is, do things normalize eventually and the normal laws of physics return.

Markets are complex and influenced by various factors like monetary policy, global events, and technological shifts. While the risk of recession is real, predicting their scale and timing remains extremely challenging. A long-term investment strategy is key in navigating such uncertainties.

This means that we simply allocate to the areas of the market that present the best opportunities. Our focus is on the bond and income side of the ledger and will typically not take big equity calls outside of shifts in asset allocations (shifting some capital towards equities and away based on medium-term RSIs).

Today, within equities, we would focus on the smaller companies and emerging markets as interest rates fall faster in the US than in developing nations.

Smalls caps experienced a recession with the index down more than 65% at its worst. It remains excessively cheap when compared to the S&P 500 index as a whole. Some of that is the larger companies ("Magnificent 7") getting super big in 2023 while the rest is small caps falling much more than mid-caps or even large caps, ex-the Mag7.

Tom McClellan:

The Fed Funds rate is now almost a full point above the 2-year yield, reflecting an immense amount of overly tight monetary policy from the Fed. They were slow to respond just like this in 2001 and 2007, and each time it caused big problems.

I think the source of the decline will be the weakening balance sheet of the consumer as their stimulus cash runs out. However, this will be coupled with a massive drag on the fiscal side as the government is forced to cut back the growth of spending.

Remember, the government rarely cuts spending. They just cut the growth of spending.

Deficits are on track to really explode over the next five years, after having already grown massively over the previous four years.

By 2025, we have a truly massive fiscal cliff approaching. Provisions of the Affordable Care Act and most provisions of Donald Trump’s tax cuts are both set to expire in 2025, and at the same time the debt ceiling will unfreeze, and the spending caps instituted under the Fiscal Responsibility Act will expire.

From Brookings:

The White House faces an uphill battle to avoid default and pursue other fiscal priorities, like taxes on the wealthy and extending parts of the Affordable Care Act, while Republicans will likely be able to again hold the entire global economy hostage. The ransom this time around may well be even more drastic. The GOP, emboldened by their victory, could try to win extensions of spending and tax cuts along with kneecapping the Democratic agenda.

I wrote not long ago that for most of the last three decades, it was the Republicans willing to "hold the US hostage" and damage the credit rating of the country for their agenda. However, that may change as the truly heroic amounts of new debt being added to future generations could sway the public to their side for once.

In any event, the outcome is likely to be similar though not the same. With a Republican congress and Democratic presidency, you are likely to see massive spending cuts- sequestration (see 2010) on steroids.

That curtailment of spending growth will create a massive fiscal drag to the economy and could cause a recessionary environment for several years in a worst-case scenario. Even if the worst-case scenario doesn't materialize the economy will slow and interest rates will slow.

Continue To Lock In These Yields While You Can

CommishJW recently posted a Barron's article by Amey Stone titled "Lock In Higher Rates on your Portfolio While You Still Can." In it they discussed what we have been doing for most of 2023- extending maturities out and buying individual bonds to LOCK IN these yields for many years to come.

For those at or near retirement, you have been handed a golden opportunity. If you thought you couldn't retire because of lower interest rates or because your hurdle rate (the rate of return you needed to achieve in order to make your retirement 'work') was too high, then that may be different today.

Interest rates are handing you an annuity-like opportunity- an income stream to last perhaps the remainder of your life- without the need to cannibalize your assets to purchase said annuity stream.

But is it too late? From the Barron's article:

Investors who are now accustomed to 5% yields on their cash may feellike they are running out of time to put money into bonds with longermaturities, something both fixed-income strategists and Barron’s [and Yield Hunting] have been recommending they do for a while now.

But it’s far from too late. “You don’t want to miss out on locking in 4%yields for five to seven years because you’re waiting to get back to 5%,”says Kathy Jones, chief fixed-income strategist at Charles Schwab.

Yes, keep some savings in those high-yielding money-market funds,but stretch into longer-term maturities as well. The main goal is to avoid the risk that when short-term rates fall, you’ll be left to reinvestat much lower rates.

“The threat of reinvestment risk becomes reality in 2024,” saysMichael Arone, an investment strategist at State Street GlobalAdvisors.

This is why we have blended and "yield-on-cost" averaged in over the last year or more into individual bonds of longer maturities to lock these yields in.

It is not too late but I would be getting a bit more aggressive here in adding new bonds. The problem is supply is fairly limited and yields are coming down fast as money flows in.

Portfolio For 2024 - Our Best Asset Allocation

In our prior letter, we laid out an asset allocation that was broken down by bond category:

Treasuries: 15%

Agency MBS: <5%

Invest Grade Corps (individuals mostly): 40%

Munis: 20%

Core Portfolio 15%

This is still a great starting point but if you haven't added treasuries yet, you will have to be satisified with a lower yield.

As I wrote last month:

Each of these components of your fixed income allocation could be "massaged" by 5%-7% on each side. In other words, treasuries could be a bit larger, especially if you're more risk averse, moving to 20%-22% of the allocation or lower to 10%-12% for the more aggressive investor.

In treasuries, you can still lock in a 4% yield floor for your portfolio that will also act as a hedge if the economy does experience a hard landing. 4%, relative to history, is not a bad floor. Here is a snapshot of treasuries with a coupon of at least 4.0% and maturity at least 7 years out.

If the coupon/income is not as much of a concern, you can get another quarter point in yield, especially if you go out a bit further in maturity.

For any of the above categories, the goal is to extend out your maturities to lock in these yields. That is not to say interest rates will never again be this high- we can't possibly know this. But we do know that the Fed is attempting to slow the economy and has telegraphed that they will be lowering rates. For the next few years at least, these rates will look pretty good in hindsight.

Since I know I will be asked, here is my current breakdown in relation to the above asset allocation:

Treasuries: 7%

Agency MBS: 3%

Individual IG bonds: 53%

Munis: 24%

Core Portfolio: 13%

For the IG bond category, the weighted average maturity is now 13.4 years and the weighted average yield-to-worst is 6.5%. In munis, this is a combination of individual munis and muni CEFs. For most of the last year, I would primarily buying individual munis but in the last two months have switched to only buying muni CEFs. That is because the upside is substantially higher in muni CEFs and the supply of decent-yielding munis has dried up.

The agency MBS was a great opportunity a few months ago but remember, those have very tight call windows so they are NOT locking in the yield. I consider that my cash allocation since the market for individual government agency bonds like Federal Farm Credit Bank ("FFCB") or Federal Home Loan Bank ("FHLB") is very liquid. I recently had a few of these called that I purchased earlier this year. The rest become callable by the end of next year and I fully expect them to be called away. At that point, reinvestment risk will likely hit me like a ton of bricks. Thus, these will be a source of cash if I have more opportunities to lock in yield in other areas.

I hope this helps members gain a foothold on their income portfolios outside of their equity allocations. REITs, preferreds, and other more 'equity-like' areas of the market can be added to complement these more traditional buckets.

Portfolio for 2024 - Our Best Ideas

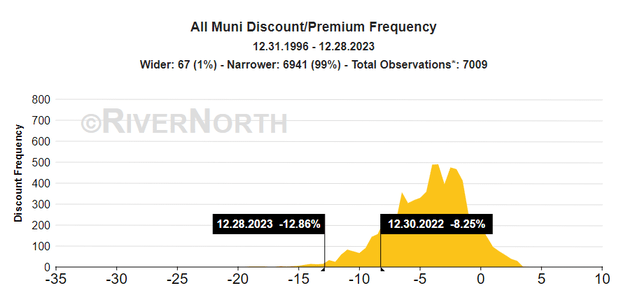

Like the Peter Tchir quote that kicked off this letter, I believe that muni CEFs are a massive opportunity today. While prices are higher than they were two months ago, in some cases substantially, the discounts remain near their widest levels ever.

At year end, accroding to RiverNorth, muni discounts have only been wider on 67 individual days going back to 1996. That is out of 7,009 days. That is only 0.95% of all observations.

The issue today is this 'Saba Effect' that has happened in the muni space over the past 4 months. This is the games by fund sponsors to 'juice' the yields at unsustainable levels in order to stave off activism, mainly by Saba Capital Management.

Now, to input a small note here. I think what Saba is doing by going after some of these fund sponsors is excellent and highly beneficial to shareholders.

Yields, for the most part, are meaningless since the fund sponsor can set the monthly payment at any level they want. It will just pay out the net investment income ("NII") plus some return of capital ("RoC") or "basis".

Right now, the highest-yielding NII funds are:

Mainstay Mackay DefTerm Muni (MMD), yield 5.24%, discount -5.64%

Abrdn National Muni Inc (VFL), yield 4.41%, discount -16.16%

Nuveen Muni Credit Opps (NMCO), yield 5.51%, discount -13.37%

Federated Premier Muni Inc (FMN), yield 3.82%, discount -13.7%

Nuveen Dynamic Muni Opps (NDMO), yield 7.52%, discount -10.16%

MFS Muni Income (MFM), yield 4.06%, discount -14.07%

Blackrock 2037 Muni Target Term (BMN), yield 4.80%, discount -9.2%

Pioneer Muni High Income Opp (MIO), yield 4.83%, discount -16.34%

Nuveen Muni Credit Income (NZF), yield 5.23%, discount -15.14%

Eaton Vance Muni Income (EVN), yield 4.58%, discount -14.3%

Blackrock MuniHoldings NJ Quality (MUJ), yield 5.26%, disc -14.51%

Eaton Vance National Muni Opp (EOT), yield 4.43%, discount -9.0%

The above list is quote large but that is by design. We want to spread our bets around to keep liquidity as many of these funds I don't want to own more than a few thousand shares, max.

This list is a good place to build a muni CEF portfolio that not only creates a long-term income stream but also stands to benefit from the potential slingshot in discounts when they tighten up.

I will attempt to name the best ideas of the day in the Daily Notes so members can keep legging into these to take advantage of the January Effect, when discounts typically tighten in January thanks to seasonal factors (rebuying after-tax loss selling, new flows into munis, etc).

Core Portfolio | A More Compelling Entry Point

We had another strong month in the Core Portfolio with gains of +3.4% on price and +3.3% on NAV. The weighted average discount is now -12.6% compared with -12.9% last month. The key takeaway is that the gains in December were driven by NAVs as we saw virtually no discount tightening.

I like the way the portfolio is positioned today with lots of 'safety' and duration- meaning a play on lower rates. That's what helped it return over 13% in the last two months.

Our top holding, Nuveen Taxable Muni (NBB) just issued a sizable special distribution of $0.4823 per share and paid on Dec 29th. The fund is up 6.82% in the month.

The only change I am making for January is to swap out Western Asset Mortgage Opp (DMO), which is trading near a 52-week high in terms of discount at -7.5%, for PIMCO Corp & Inco Strategy (PCN).

PCN is now trading at a 6% premium, an area it has traded only a handful of times going back to the start of the century. The fund is also fairly liquid with 168K shares traded daily and has had nice NAV momentum.

This is a great buy-and-hold fund.

For those who want to keep the portfolio size more manageable, you can substitute in PCN for any of the other PIMCO positions, save for PDX, which is a special situation fund.

Housekeeping Items

Please note that the Google Sheet is new this month as it is every month. There is a date at the top in the title of the sheet as well as the date in the spreadsheet itself. On the first of each month, we create a new sheet and link.

New members should start with the following informative reports:

On the Google Sheet, we have an "Instructions" tab as a quick guide for more novice investors. Also, please don’t hesitate to email us with any questions at Admin@Yieldhunting.com.

Fun With Charts

1) International stocks are VERY cheap relative to US stocks.

2) Conference board's leading economic indicators still are moving lower.

3) Small caps look really good here.

4) I don't think the state of the consumer and the retrenchment of credit is getting nearly enough play in the media:

5) For my members, i hope this is going the other way.

6) Strategists were very wrong in 2023 and now are jumping over each other to increase their target for 2024. Will they be wrong the other way this year?

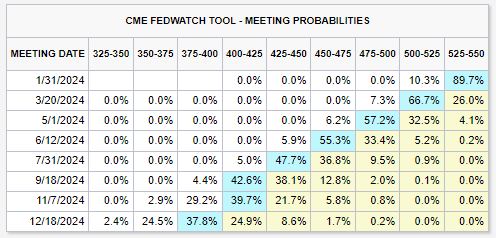

7) The March meeting sees a 70%+ chance for the first cut in the Fed Funds rate.

8) The Goldman Financial Conditions Index has hit its lowest point of 2023, which should be good news for companies that need to roll debt or go public.

9) Scary chart on the left. Not so scary chart on the right. This is the same set of data.

10) Want some light reading? Here are a bunch of outlooks from select banks and investment shops.

BANKS (US)

J.P. Morgan: https://shorturl.at/eltPT

J.P. Morgan Private Bank: https://shorturl.at/eyzHK

Goldman Sachs:https://shorturl.at/gqLX2

Goldman Sachs Asset Management: Asset Management Outlook 2024: Embracing New Realities

Morgan Stanley:2024 Investment Outlook: Thread the Needle | Morgan Stanley

Bank of America: BofA Global Research Calls 2024 "The Year of the Landing"

Bank of America Private Bank: 2024 Economic & Market Outlook: How Investors Can Prepare

Wells Fargo: https://t.ly/2bF1E

BNY Mellon: https://t.ly/BCLLT

State Street:https://t.ly/p47tE

Lazard: https://t.ly/ZkkUm

T. Rowe Price: https://t.ly/e9b3d

TD Securities: 2024 Global Outlook: Ready, Set, Slow

Charles Schwab: 2024 Global Outlook: The Big Picture

RBC Capital Markets: 2024 Global Macroeconomic Outlook

BANKS (EUROPEAN)

UBS: The Year Ahead

Deutsche Bank: LinkedIn

BNP Paribas: LinkedIn

Barclays: LinkedIn

Lombard Odier Group: LinkedIn

Macquarie Group: LinkedIn

ASSET MANAGERS

BlackRock: https://lnkd.in/eSxDA_bR

Amundi: LinkedIn

M&G plc: LinkedIn

Man Group: LinkedIn

Wellington Management: LinkedIn

Invesco US:LinkedIn

Legal & General Investment Management (LGIM): LinkedIn

Schroders: LinkedIn

Deutsche Bank (Wealth): LinkedIn

Allianz: LinkedIn

AXA IM: LinkedIn

PIMCO: LinkedIn

Capital Group: https://lnkd.in/ehH2jW3a

Julius Baer (secular outlook): LinkedIn

Pictet: LinkedIn

Vanguard: LinkedIn

Fidelity: LinkedIn

Cambridge Associates: LinkedIn

PRIVATE EQUITY

KKR: LinkedIn

Apollo Global Management, Inc: LinkedIn

Blackstone: LinkedIn

BlackRock (Private Markets): LinkedIn

AUDIT & CONSULTING

@HayekAndKeynes