How I'm Building A Tax-Free Portfolio With 8% Yields And Double Digit Total Returns

Public

Summary

CEFs continue to provide an advantage over most open-end and passive options in the fixed income category. If placed into a ROTH IRA, then it will never be taxed.

While more volatile than traditional fixed income, we typically take a counter-cyclical approach by buying over time ("DCA") during periods of volatility.

By compounding in a tax-deferred or tax-free setting, you can greatly accelerate your account values. So holding your most aggressive income-producing assets in ROTHs makes the most sense.

High quality and well-run CEFs are fantastic "buy-and-hold" investments but to produce additional alpha, we suggest a "buy-and-rent" approach of buying the dips and reducing at rich valuations.

Introduction

Similar to a REIT, the majority of Closed-End Funds ("CEFs") are regulated as "RICs" or registered investment companies. That requires them to distribute to shareholders at least 90% of their annual taxable income to shareholders, avoiding corporate income or an excise tax before paying shareholders. The structure prioritizes income to shareholders (rather than focusing on capital appreciation). That along with other structural advantages of CEFs give them yields in excess of 6-10%.

For those that love the details and/or need some good material to help them fall asleep, you can read more about the statutory and regulatory requirements for CEFs HERE.

The distributions paid by taxable bond CEFs are reported via 1099-DIV statements and tax as ordinary income. This is why we discuss so frequently where to place certain CEFs. Ordinary income producing assets should be placed into a ROTH or traditional IRA whenever possible. We then place our equities into our non-qualified ("taxable") brokerage accounts.

For those in distribution mode, that may not be an easy thing to do and tax strategy will then play an important role. That is because traditional income distribution planning would suggest you pull from your taxable account first and then from your qualified (IRAs, 401K, etc) last. This is to allow your tax-deferred accounts to compound as much as possible.

The CEF Wrapper

There are several key concepts investors need to consider when investing in CEFs. For one, the CEF wrapper is what I call the "Anti-Wall Street Investment." This is because Wall Street, while making some money from them, does not nearly make as much as they would in an open-end fund (a mutual fund or an ETF).

The main differentiating characteristic of a CEF is their structure. They typically raise capital through an Initial Public Offering ("IPO") by issuing shares just once. Generally speaking, the number of shares is thus fixed, hence the "closed" nomenclature (they can buyback shares and they can, under unique circumstances, issue new shares).

Since the shares are fixed, they can trade at a premium or discount to Net Asset Value ("NAV"). What is NAV? If you liquidate all the holdings in the portfolio that is what each shareholder would get per share. Without new shares being created, anyone buying into a CEF means they are buying from someone who is selling their shares. Traditional supply and demand.

Since it is based on a market, the share price can deviate from the NAV (or true value of the fund). Mutual funds and ETFs can employ mechanisms like market-makers to ensure that the price stays at or near the NAV. All else equal, a CEF allows a shareholder to buy assets for a discount to where they are trading giving them the potential for capital gains and a higher yield.

The Advantage Of CEFs

There are many built-in advantages of CEFs but we will focus on just the few main ones. The first is that the lack of cash flows reduces performance drag. Constant inflows and outflows of mutual funds and ETFs 'force' the portfolio manager to sell when they otherwise would rather be buying and buy when they otherwise would want to sell. That is a friction not inherent in CEFs.

Second, leverage is a key benefit for CEFs that is not apparent in mutual funds or most ETFs. These funds borrow short and invest long "earning the spread." While leverage works both ways, amplifying gains as well as losses, studies show that CEFs that use leverage produce an advantage over those that do not 15 out of the last 20 years.

Third, you receive higher yields in a yieldless world. 14 years ago, you could have invested in a six-month CD and produced a 5%+ yield. Today, those same CDs yield less than 0.5%, for a 90% loss in income. Some of that higher yield stems from them being able to invest in less-liquid bonds. Liquidity carries a premium in the bond world since some bonds trade only by appointment. As such, bonds that rarely trade tend to have higher yields. With no cash flows (the fund is closed), they can hold many illiquid bonds and produce higher yields, all other risks held equal.

(Source: Blackrock)

Fourth, the ability to buy shares at a discount produces "free yield." Just like when you buy a dividend stock at a lower price produces a higher dividend yield, buying a CEF at a wider discount will produce a higher distribution yield. This is a key advantage as that free yield can, in many cases, completely offset the management fees so you get the fund management for free.

Fifth, mean reversion is your friend. While a stock is worth what the market thinks it is worth, a bond CEF has a true value in that NAV mark. Studies show that over time, discounts revert to long-term average. This gives investors the opportunity to juice their returns through capital gains. And they get paid the higher yields while they wait.

Better Returns Over Time

One thing I've stressed to investors is to create a diversified income stream. That is diversification of income, not just of assets. Those income streams should come from many differing, and where possible, uncorrelated sources.

CEFs can be volatile on price and the best way to invest in these income vehicles is through dollar averaging the purchases during general market pullbacks or idiosyncratic fund sell offs.

Investing in the CEF space makes sense if you want to hold a fixed income allocation in your portfolio. Today, investment grade bonds, treasuries, and most mortgages offer almost nothing in terms of yields. So investors are likely venturing out into higher risk areas including adding more to their dividend stock portfolios for income.

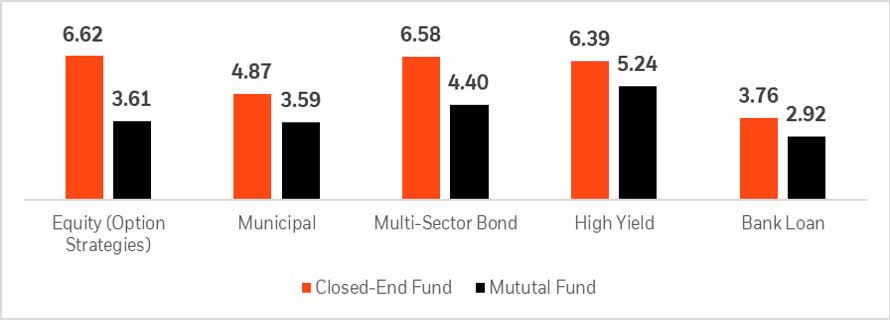

But CEFs can return much better than traditional mutual funds within the main fixed income sub-sectors:

Five Year Total Returns By Category:

(Source: Blackrock)

We looked at all 112 taxable CEFs and compared them to a few passive ETFs that focus on higher yields. I know these are popular tools for income investors as I get questions and comments on them all of the time. They include:

Vanguard REIT ETF (VNQ)

SPDR S&P Dividend ETF (SDY)

Vanguard High Dividend Yield Index (VYM)

SPDR Portfolio S&P 500 High Dividend ETF (SPYD)

Global X US Preferred ETF (PFFD)

Global X Superdividend US ETF (DIV)

iShares High Yield Bond (HYG)

Alerian MLP ETF (AMLP)

Of the 112 taxable CEFs that were around at the end of 2018, 56 beat the S&P 500 Div Index. For bond funds, that is a fairly strong track record.

(Source: Alpha Gen Capital)

We Use A Counter-Cyclical Approach

CEF pricing can be volatile which can be a good thing for investors who watch these things closely and take advantage of both oversold assets as well as funds that have skyrocketed. One of our first articles on the subject of closed-end funds was titled "How To Measure Closed-End Fund Risk." Specifically, the "How To Look At Price Volatility" section.

But what if you look at all the price volatility as an opportunity? After all, if the true value of the fund is the NAV and the prices are simply a reflection of daily trading imbalances or unsophisticated sentiment, shouldn't you assess prices as opportunities to buy or sell? Any day when there's a 1%+ move in a CEF can be thought of as a day when there is a supply and demand imbalance (outside of ex-dividend days and large moves in interest rates). The NAV of a typical CEF moves less than 50 bps even on volatile days - and most days likely less than 20 bps.

So thinking of price volatility as an opportunity is imperative to producing better outcomes in your income portfolios. If you can think of a fast-dropping price relative to the NAV as an opportunity rather than becoming fearful, and buy when there's a sea of red on your screen, you will be buying at the best times in many cases.

As the image below shows, in rich CEF environments, meaning that discounts are relatively tight, we want to be rotating out of CEFs and into discount-less risk options. These are passive income vehicles like ETFs or into bond mutual funds.

We loaded up on CEFs starting back in late September and really through the end of 2020. Discounts were wide as investors were risk weary because of the upcoming election and potential for a contested outcome.

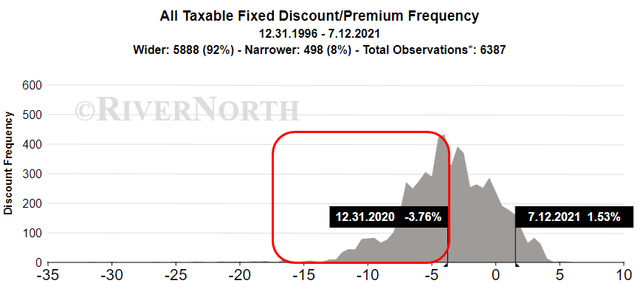

Below is the distribution bell curve of the taxable bond CEF group going back to 1996. Today, valuations are in the top 8% of all observable outcomes with an average premium of 1.53%. Back at the start of the year, the average taxable CEF traded with a -3.8% discount.

We want to be buyers of taxable CEFs in large quantities when we are in the red box, i.e. the left side of the distribution.

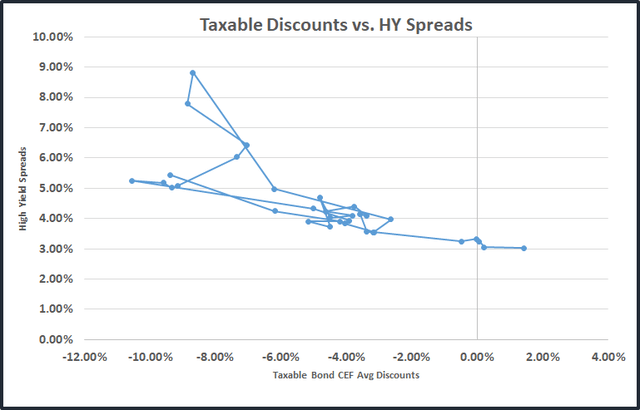

Put another way, we want to be buyers when discounts are wide. But not only that, we want to invest when discounts are wide AND credit spreads are wide. Credit spreads are the amount of additional income received over and above the same maturity treasury rate. When we are in a highly volatile time, credit spreads will blow out, at the same time discounts blow out.

The chart below maps credit spreads and taxable CEF discounts over the last 2.5 years. Whenever the data point is in the top left, that is when you want to buy. When we are in the bottom right, those are times to think about reducing exposure or at a minimum not adding to exposure (if you are a buy and hold investor/ living off the income).

You can guess which monthly dates were in the top left (March, April 2020) and which are in the bottom right (most recent)

Summary, Recommendations and Tax-Advantage Accounts

We believe interest rates will remain low for some time and that all the retiring baby boomers (10,000 per day!) will need income to sustain their lifestyles into retirement. Most workers in the late 50s through mid-60s are failing to comprehend just how much additional capital they need to generate the same amount of income.

CEFs pay a higher than average yield and patient investors can get even better total returns by taking advantage of volatility and employing a counter-cyclical approach. For investors who are looking to build a CEF portfolio, please consider the following suggestions:

Invest in higher quality bond CEFs. Equity CEFs, while paying juicy yields, offer no advantage over passive vehicles. They do not employ leverage and they have higher fees.

Do NOT buy based on discount and yield in nearly every environment. Most CEFs are retail investor owned who tend to solely look at discounts and yield for their investment decisions.

Diversify! Have at least 5 different bond CEFs in your portfolio and up to 15. Having a wide variety can help buffer single-CEF risks.

Use limit orders only! CEFs have limited order books so by placing a market order you can blow through those orders and send a price shooting higher.

Have patience! It is important for new investors to be patient and start with a smaller amount of shares getting into positions in tranches. This will allow investors to follow the name and get familiar with how it trades.

Why Using A Roth Makes Most Sense? The Magical Benefits

The Roth IRA is a special account type made up of after-tax dollars that grow tax-deferred and come out tax-free. No other account type does that except the death benefit from life insurance.

Contributions are NOT tax-deductible so they are made with after- tax dollars. This is why we typically have younger folks who are earning money to use the Roth as well as retirees who still have some earned income.

After the age of 59 1/2 you can start withdrawing the money tax-free. Roth accounts can make great stop-gaps for people who retire early and are not yet at Social Security ("full retirement age") or at the age where they are required to take distributions from a traditional IRA.

Roth IRAs have no required minimum distributions and you can leave the capital in there as long as you live.

Today, you can contribute $6,000 per year into a Roth but if you're over the age of 50, you can do up to $7,000. The one issue is that you cannot contribute to a Roth if your aggregate gross income is over $208K (married filing jointly) or more than $140K if you file as a single.

The Roth is the ultimate account type because it has so much flexibility. You can take money out if needed without penalty and taxes. But most importantly, you do not have to worry about the potential for higher taxes down the road.

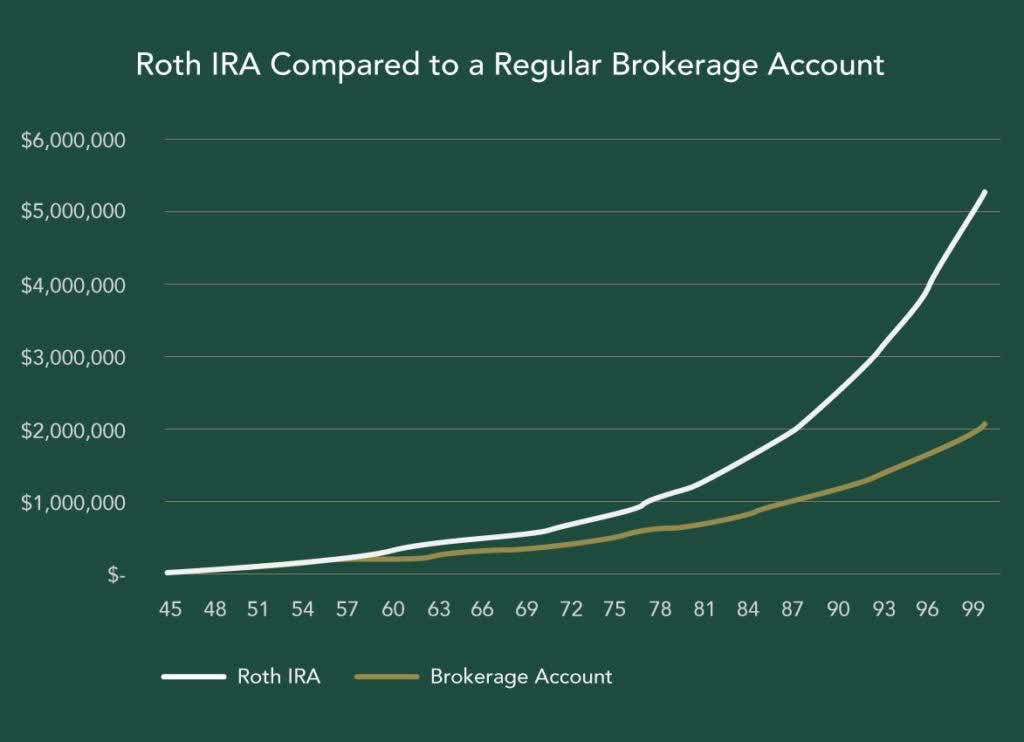

By placing your 'aggressive' income producing assets into your Roth, you will never be taxed as long as you don't withdraw it before 59.5. That means you do not have to withdraw money to pay for taxes like you would in a non-qualified "taxable" account. Allowing money to compound faster without having to pay taxes can make a massive difference in outcomes. Check out the image below that shows the account balance of a Roth vs. a taxable account with the same contributions and same annual return. The Roth ends up with 3-times the capital after 40 years.

(Source: wjohnsonassociates.com)

Concluding Thoughts

We continue to be patient waiting for the next great buying opportunity in closed-end funds and other higher-yielding assets. For now it makes sense to sit tight but not in cash - as it yields nothing. We do not see a catalyst for credit spreads blowing out in the near-term so we want to participate in the NAVs continuing higher, but with income vehicles that will not see discounts widen.

Additionally, we have a report coming out where we highlight what we think will be the upcoming catalyst to much wider discounts.

Over the next few weeks, we will continue to highlight relative value trades to make in your portfolios to take advantage of idiosyncratic dislocations.